SB News - September 2025

Chip Wars

In a recent move aimed at gaining technological sovereignty, China has ordered domestic tech firms to stop buying key Nvidia’s artificial intelligence (‘AI’) chips, escalating its efforts to develop a Chinese semiconductor industry that is less reliant on US influence. The chip ban, which includes Nvidia’s made-for-China H20 AI chip, comes at a time when there is increasing Chinese government confidence that its homegrown processors can rival Nvidia’s AI chips.

The directive, issued by China’s cyberspace regulator, specifically instructs companies like Alibaba and Tencent to stop buying and testing Nvidia’s H20 and RTX Pro 6000D AI chips. The move follows a national security review of the H20 chip initiated in August over concerns it could contain tracking systems. Several Chinese companies, that had tested or placed large orders for these chips, were told to immediately cease purchases. Adding to Nvidia’s challenges, Chinese regulators have also launched a preliminary anti-monopoly probe into the US chip giant.

This ban is the latest chapter in a deepening technology rivalry between China and Western countries and is consistent with the China’s ‘Made in China 2025’ policy which encourages increased production in high-tech products and services, with China’s semiconductor industry central to its industrial plan. US export controls, first imposed in 2022, blocked Chinese access to Nvidia’s top-tier A100 and H100 chips, which are crucial for training advanced AI models. Nvidia responded by creating downgraded versions of its chips specifically for the Chinese market, like the H20, which were deliberately restricted to comply with US export controls. However, Beijing now appears to be rejecting these lesser chips, urging companies to “double down on local innovation” instead.

Wei Shaojun, a senior Chinese government adviser and vice president of the China Semiconductor Industry Association, publicly called for the nation to ditch Nvidia chips, warning that reliance on US hardware poses a “lethal” long-term risk. He argued that China must stop imitating US chips and instead innovate at the silicon level. This goal is being aided by the Chinese government’s US$100 billion National Integrated Circuit Industry Investment Fund that aims to help China reach its national goal of achieving self-sufficiency in the semiconductor industry by investing in domestic semiconductor companies.

Fuelling confidence in China’s semiconductor industry is the emergence of domestic AI chip alternatives from companies like Huawei and Alibaba. In a widely publicised demonstration on Chinese state television, Alibaba’s new “PPU” AI accelerator chip was benchmarked against Nvidia’s H20, with a chart implying performance parity. The broadcast revealed that state-owned China Unicom has already deployed over 16,000 of Alibaba’s PPU chips in a massive new data centre. Meanwhile, Huawei’s forthcoming Ascend 910C chips are being positioned as a powerful homegrown Nvidia rival. Major Chinese companies including Baidu, ByteDance and China Mobile have reportedly tested the 910C and according to Huawei, the device is on par with Nvidia’s flagship H100 chip which isn’t available in China.

Some analysts view Beijing’s actions as a strategic negotiation tactic aimed at both fostering self-reliance and gaining leverage in broader trade talks with the US. While domestic chip manufacturers still face significant challenges in scaling up chip production to meet strong Chinese demand, the message from the Chinese government is clear: the era of dependence on foreign technology is ending. The government is pushing its national champions to build the foundations for a self-sufficient future with supply chain and geopolitical resilience as well as industry dominance where the world’s AI runs on lower cost Chinese silicon chips and open source AI models such as those developed by DeepSeek.

By Nick Ryder, Chief Investment Officer

TikTok and the Tech Cold War

President Donald Trump’s executive order approving a deal to keep TikTok operational in the United States is not merely a regulatory manoeuvre. It is a strategic intervention in the broader contest for technological dominance between the U.S. and China. The order enables a consortium of American investors to take majority control of TikTok’s U.S. operations, addressing national security concerns while reshaping the financial structure of one of the world’s most influential digital platforms.

The deal values TikTok’s U.S. business at USD $14 billion, a figure significantly below previous market estimates of USD $30 to $35 billion. Analysts suggest this valuation reflects political compromise rather than intrinsic market fundamentals. Oracle, Silver Lake and the Abu Dhabi-based MGX investment fund will hold a combined 45% stake, while ByteDance investors and other new investors retain 35%. ByteDance itself will hold 19.9% percent, satisfying the divest-or-ban law passed in 2024.

From a financial markets’ perspective, the transaction is notable for its structure and timing. No federal equity stake or “golden share” is involved, meaning the U.S. government will not directly influence TikTok’s governance. Instead, control will rest with private investors, many of whom have close ties to Trump, including Oracle co-founder Larry Ellison. This has seen some commentators raise questions about editorial independence and the potential for political influence over content moderation.

Oracle’s role is central. It will oversee TikTok’s security operations and retrain a licensed copy of the recommendation algorithm using U.S. user data. This retraining is intended to nullify risks of Chinese interference, though the original algorithm remains under ByteDance’s ownership. The lack of full algorithmic control has drawn criticism from lawmakers who argue the deal may not fully comply with the Protecting Americans from Foreign Adversary Controlled Applications Act.

The economic implications extend beyond TikTok. The deal is emblematic of a broader U.S. strategy to decouple from Chinese technology. Export controls on semiconductors, AI chips and cloud infrastructure have already reshaped global supply chains. The CHIPS Act has funnelled billions into domestic manufacturing, and the TikTok deal reinforces the message that software platforms are now viewed as strategic assets. China’s response has been muted. While President Xi Jinping reportedly gave informal approval, Beijing has not formally endorsed the deal. Analysts suggest China’s motivation is pragmatic. As Dimitar Gueorguiev of Syracuse University notes, Beijing is prioritising access to U.S. technology and services to build self-sufficiency in semiconductors and AI. TikTok, by contrast, is a maturing consumer app with diminishing strategic weight.

The economic implications extend beyond TikTok. The deal is emblematic of a broader U.S. strategy to decouple from Chinese technology. Export controls on semiconductors, AI chips and cloud infrastructure have already reshaped global supply chains. The CHIPS Act has funnelled billions into domestic manufacturing, and the TikTok deal reinforces the message that software platforms are now viewed as strategic assets. China’s response has been muted. While President Xi Jinping reportedly gave informal approval, Beijing has not formally endorsed the deal. Analysts suggest China’s motivation is pragmatic. As Dimitar Gueorguiev of Syracuse University notes, Beijing is prioritising access to U.S. technology and services to build self-sufficiency in semiconductors and AI. TikTok, by contrast, is a maturing consumer app with diminishing strategic weight.

For investors, the deal offers both opportunity and risk. The new TikTok entity will be American-operated, but its success depends on user retention, regulatory stability and geopolitical cooperation. Any disruption to the algorithm or user experience could erode market share. Moreover, the involvement of politically connected investors introduces reputational risk and potential volatility. The TikTok executive order is a financial and geopolitical pivot point. It reflects the U.S. intent to assert control over digital infrastructure while navigating the complexities of global capital, national security and technological sovereignty. The outcome will shape not only TikTok’s future, but also the contours of the next decade in digital economics.

Sources: Bloomberg & CNBC

By Vincent O’Neill, Chief Executive Officer

ASIC Puts Private Credit on Notice After Damning Review

Australia’s private credit sector has been dealt a sharp warning after the corporate regulator released a report exposing systemic weaknesses across the fast-growing $200 billion industry. The review, commissioned by ASIC, painted a picture of a market expanding faster than its governance and disclosure practices can support.

The regulator pointed to widespread shortcomings in how funds communicate risk, value illiquid assets and structure products for retail investors. In some cases, the target market documents meant to guide who a product is suitable for were little more than boilerplate. In others, fee structures and redemption features gave a rosier impression than the underlying loan portfolios justified. ASIC also highlighted concerns around related-party lending in development finance and the concentration of decision-making power with managers rather than independent boards.

While La Trobe Financial has become the most visible example, with temporary stop orders placed on several of its products last week, the message from ASIC was that these problems are sector-wide. La Trobe’s setback is awkward for its owner Brookfield, which has been running a sale process, but the regulator’s findings go well beyond a single firm.

ASIC chair Joe Longo described the report as a turning point, stressing that private credit managers must “lift their standards” in disclosure, valuation and governance. For funds that have relied on opaque valuation models or marketed themselves on yield while glossing over illiquidity, today’s report suggests those practices will no longer pass muster.

The implications are two-fold. For managers, there will be a scramble to tighten governance, strengthen documentation and adjust how risks are communicated. For investors, especially those in retail-accessible vehicles, the report is a reminder to scrutinise how funds are priced, how liquidity is managed and whether the product’s profile genuinely matches their own risk appetite.

The rapid growth of private credit has made it an increasingly important part of Australia’s capital markets. But with that growth has come scrutiny. ASIC’s review signals that the era of light-touch oversight is ending, and that private credit will now be held to the same disclosure and governance standards as other mainstream asset classes.

By Joey Mouracadeh, Senior Investment Director

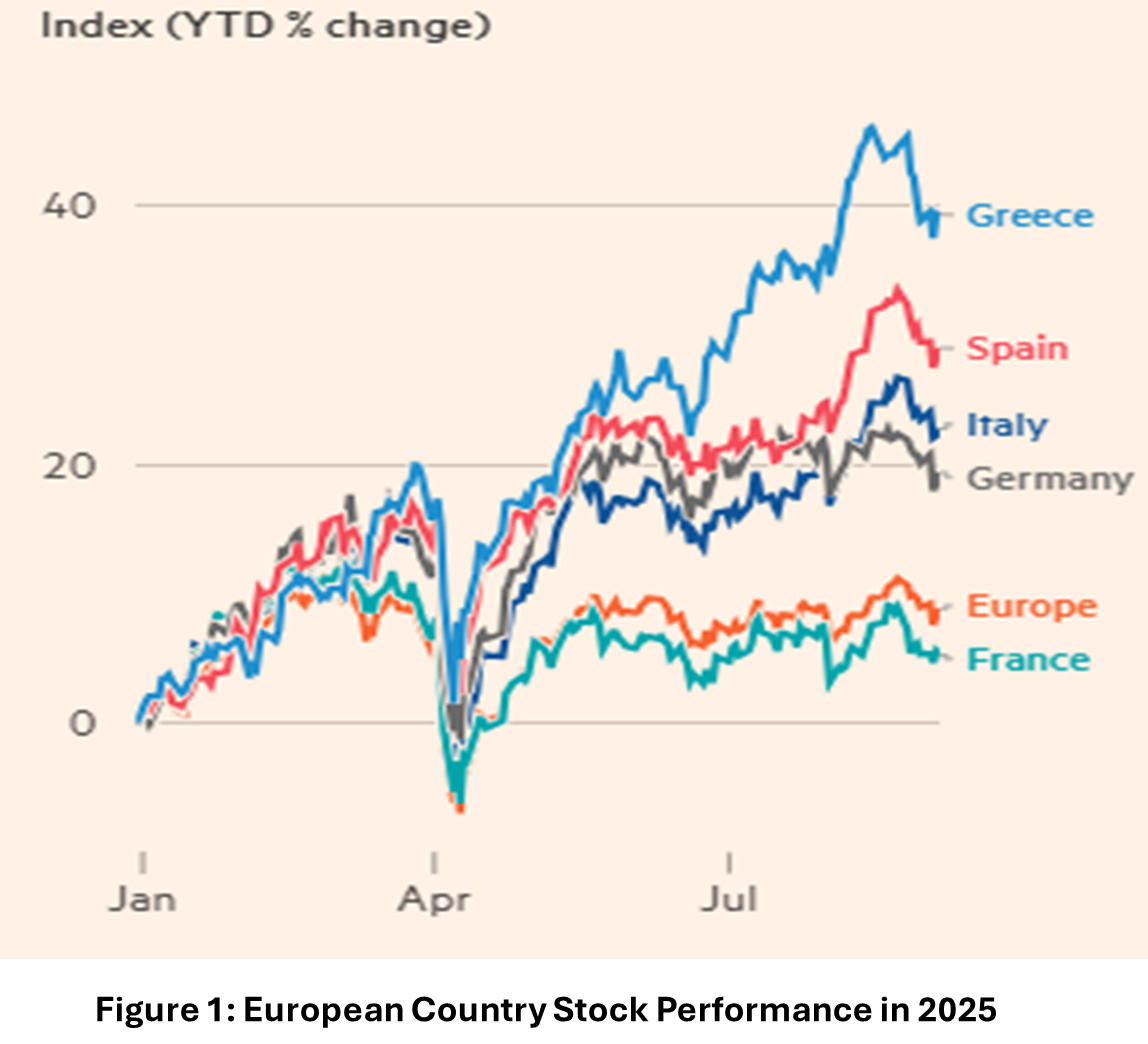

Southern Europe’s Stock Markets Surge, Outperforming Their Major European Peers

Southern Europe’s once overlooked stock markets are now leading the charge across the continent, capturing investor attention as they seek value amidst a renewed wave of enthusiasm for European equities. This year, equity markets in Greece, Italy, and Spain; countries once at the heart of Europe’s debt crisis, have surged past their larger counterparts in Germany and France, even outperforming the broader Stoxx Europe 600 index.

A key factor driving this shift is the perceived valuation gap that exists between the equity markets in these countries. Southern European markets began the year trading at significantly lower price-to-earnings ratios than the German and French indices, offering investors a more affordable entry point into Europe’s growth story. A growth story being fuelled by a dramatic boost in European defence spending, off the back of President Trump’s demands for NATO allies to increase their contributions to the alliance. In addition, uncertainty surrounding President Trump’s trade policy has spurred some investors to begin diversifying part of their portfolio away from the US.

Italy, Spain, and Greece have outpaced most other European markets so far this year. This has been underpinned by strong economic fundamentals as the second quarter of 2025, saw Greece’s economy expand by 1.7% year-on-year, in stark contrast to Germany’s GDP contraction of 0.3%. Southern European markets are also more domestically focused, insulating them from the impact of US tariffs and the uncertainty they have caused in global markets. On the other hand, countries like Germany are heavily exposed to the US and Asia and are much more vulnerable to global trade disruptions. Likewise, France’s equity markets have also been troubled mainly due to political turbulence which ultimately led to a government collapse earlier this month.

Homing in closer, the composition of southern European equity markets has also played a role in their outperformance. The financials sector represents a significant portion of these markets, making up 50% of Italy’s FTSE MIB and 44% of the Athens Stock Exchange. By contrast, financials comprise just 8.6% of the broader Stoxx Europe 600 Index. European banks have enjoyed a remarkable rebound this year, with share prices hitting levels not seen since the global financial crisis. Sustained higher interest rates have boosted bank revenues, while improving economic sentiment and cheap valuations have attracted investors. This has seen the financial sector (MSCI Europe Financials Index) return over 37% in the twelve months to the end of August 2025, far surpassing the broader Stoxx Europe 600 Index which has roughly returned 8% over the same period.

The wide dispersion of returns, not only within European markets but also across its various sectors, underscores the importance of maintaining broadly diversified portfolios. In today’s environment, where abrupt policy shifts (such as tariff decisions under the Trump administration) can trigger significant market dislocations, diversification becomes both a risk management tool and a source of opportunity. While the US economy remains fundamentally strong, partnering with equity managers who can identify and access opportunities beyond the US is increasingly vital. With US equity valuations reaching new highs and becoming more expensive, the ability to selectively pivot toward more attractive global opportunities can be considered a strategic advantage.

By Joey Nakhoul, Investment Research Analyst

Home Prices

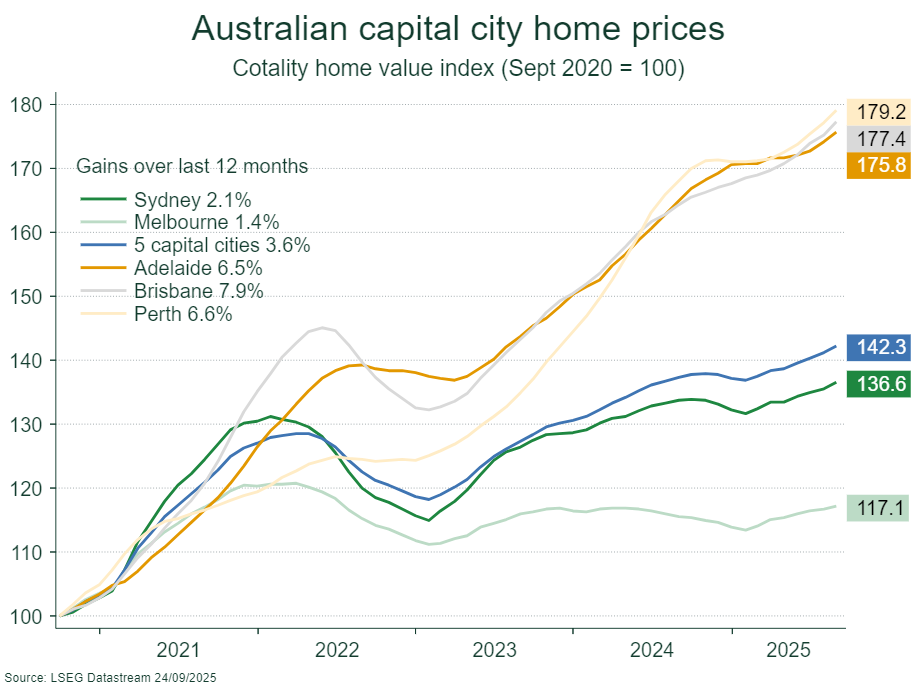

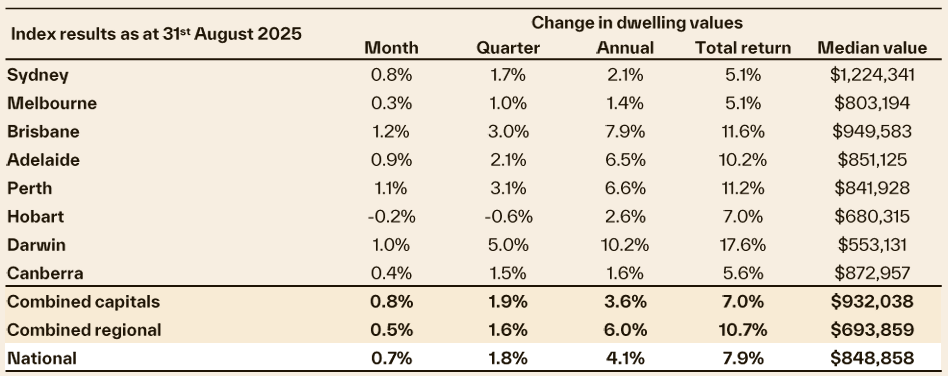

Australian home values rose 0.7% in August, the strongest monthly gain since May 2024 — pushing annual price growth to 4.1%, according to the Cotality (formerly CoreLogic) Home Value Index. Momentum in home prices has been building since the RBA began cutting interest rates in February with lower interest rates and slower inflation helping to boost demand through increased borrowing capacity, real wage growth and buyer confidence. Meanwhile the number of homes advertised for sale is around 20% lower than the average for this time of year which has seen auction clearance rates rise to 70%, the highest since February 2024. The home price growth trend remains broad-based with most regions showing monthly price growth except Tasmania, where prices in Hobart fell 0.2% over the month. The mid-sized capitals continue to lead with Brisbane (+1.2%), Perth (+1.1%) and Adelaide (+0.9%) showing the strongest monthly rises. Darwin continues to show strong growth with a 1.0% rise in August and 10.2% over the year. Melbourne remains the weakest capital city with prices up only 0.3% in August and 1.3% over the past year and home prices are still 3% below the peak in March 2022.

The home price growth trend remains broad-based with most regions showing monthly price growth except Tasmania, where prices in Hobart fell 0.2% over the month. The mid-sized capitals continue to lead with Brisbane (+1.2%), Perth (+1.1%) and Adelaide (+0.9%) showing the strongest monthly rises. Darwin continues to show strong growth with a 1.0% rise in August and 10.2% over the year. Melbourne remains the weakest capital city with prices up only 0.3% in August and 1.3% over the past year and home prices are still 3% below the peak in March 2022.

According to Cotality, rental vacancies remain near record lows at around 1.5% which compares to the average vacancy rate of 3.3% in the five years before the COVID pandemic. This has seen rents rise 0.5% in August, the largest rise since May last year, and the annual rate of rental growth has now risen back up to 4.1% which could feed into official CPI inflation numbers with a lag. Gross capital city rental yields are below current mortgage rates and range from 3.0% in Sydney to 6.5% in Darwin and suggest that it is more attractive to rent than buy despite the sharp increase in rents over the past few years.

According to Cotality, rental vacancies remain near record lows at around 1.5% which compares to the average vacancy rate of 3.3% in the five years before the COVID pandemic. This has seen rents rise 0.5% in August, the largest rise since May last year, and the annual rate of rental growth has now risen back up to 4.1% which could feed into official CPI inflation numbers with a lag. Gross capital city rental yields are below current mortgage rates and range from 3.0% in Sydney to 6.5% in Darwin and suggest that it is more attractive to rent than buy despite the sharp increase in rents over the past few years.

The most recently Reuters Poll of property market analysts and economists upgraded median expectations for housing price growth in 2025 from 4.0% to 5.0%, with expectations of 5.6% price gains in 2026 and 4.8% in 2027. On the one hand, price growth is likely to be assisted by expectations for one or more rate cuts over the next year but weak affordability, slowing wage growth and lower levels of immigration are likely to place a speed limit on price growth over the next few years.

By Nick Ryder, Chief Investment Officer

Latest Podcast

SB Talks: TikTok towards a US Government Shutdown

In this episode of SB Talks, CEO Vincent O’Neill and CIO Nick Ryder, dive into a pivotal moment for global markets as 16 central banks, led by the U.S. Federal Reserve, prepare for critical policy decisions. With rate cuts back on the table, inflation still sticky, and labor markets showing cracks, what lies ahead for monetary policy? They unpack the political tension behind the Fed’s independence, the looming U.S. government shutdown, and the uncertain future of U.S.-China trade talks, starting with TikTok.

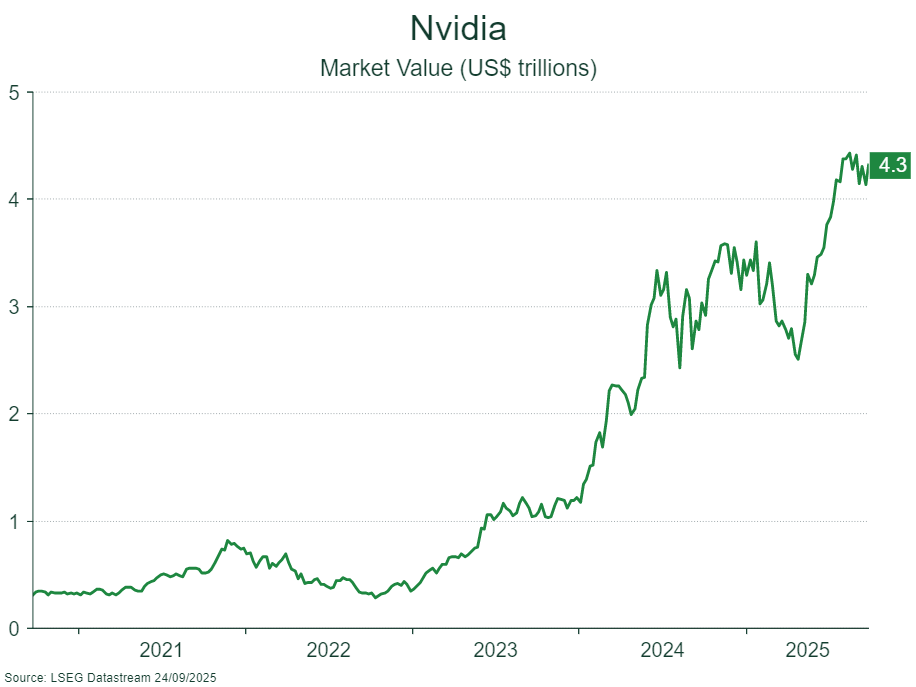

Meanwhile, Wall Street’s AI euphoria shows no signs of slowing, with tech giants surging past $3 trillion valuations.

Listen on Apple Podcasts

Watch on Youtube: