SB News - October 2025

US Bank Results Signal Reopening for Private Equity and Consumer Resilience

The global reliance on the seventeen rare earth elements (REEs) – a group comprising the fifteen lanthanides along with yttrium and scandium – rests on a profound paradox. Although these elements are moderately abundant in the Earth’s crust, the concentrated deposits necessary for mining these economically are limited in number, making viable mines relatively rare compared to other commodities. With total revenue for the global REE market estimated to be US$3.7 – 6.5 billion in 2024, the small market size makes it is difficult to economically justify development of expensive new mines and processing plants.

These rare earth materials are, however, indispensable for modern defence systems, advanced energy technologies, and high-performance permanent magnets, such as those made from neodymium-iron-boron, which are vital for electric vehicles and wind turbines. Rare earth magnets are about ten times more powerful than common ceramic magnets such as those people use to attach notes to refrigerators.

China leveraged this critical supply chain vulnerability through decades of strategic policy: Beijing declared REEs a protected resource in 1990 and subsequently provided significant subsidies and regulatory freedom, which allowed domestic producers to operate at drastically lower costs than their Western counterparts who faced strict environmental compliance. This regulatory arbitrage, combined with rapidly increases in exports that drove global prices down, successfully squeezed competitors out of the market throughout the 1990s and early 2000s.

This historical context explains why China now dominates the most strategic parts of the rare earth value chain. While it accounts for roughly 70% of global rare earth mining, its leverage is maximised downstream, controlling approximately 90% of the world’s separation and processing capacity and holding a massive 94% market share in sintered permanent magnet manufacturing, a share that stood at 50% two decades ago. Its processing capabilities are China’s true strategic bottleneck, determining final product availability regardless of where the raw ores are mined.

Developing parallel processing capacity outside China comes with immense technical and environmental challenges. Converting raw ores into usable compounds requires very specialised facilities, substantial capital investment, and accumulated technical expertise that cannot be rapidly replicated. Moreover, refining rare earths involves the use of strong acids and high temperatures, resulting in complex chemical waste streams and potential groundwater contamination. Compounding this difficulty, REE deposits often contain radioactive byproducts, requiring elaborate and costly storage and disposal solutions that stringent Western environmental regulations mandate, effectively reinforcing the competitive economic advantage China built through years of less rigorous oversight.

In response to growing technological rivalry, Beijing has accelerated the weaponisation of its market dominance. Building on supply restrictions initiated around 2010, recent governmental notifications in 2025 and late 2023 have imposed comprehensive export controls on technologies crucial to rare earth mining, separation, metal smelting, and magnetic material manufacturing. Because Chinese firms possess proprietary know-how, controlling the outflow of this expertise is aimed directly at frustrating Western attempts to develop independent capacity.

Beijing has also recently introduced an extraordinary measure of extraterritorial jurisdiction: foreign operators transferring permanent magnets between third countries must now obtain a Chinese export license if the value of specific controlled rare earth elements contained within them constitutes no less than 0.1% of the product’s total value. This low threshold allows China to assert regulatory control over a vast portion of the global downstream magnet market which are required for high-performance defence and industrial components.

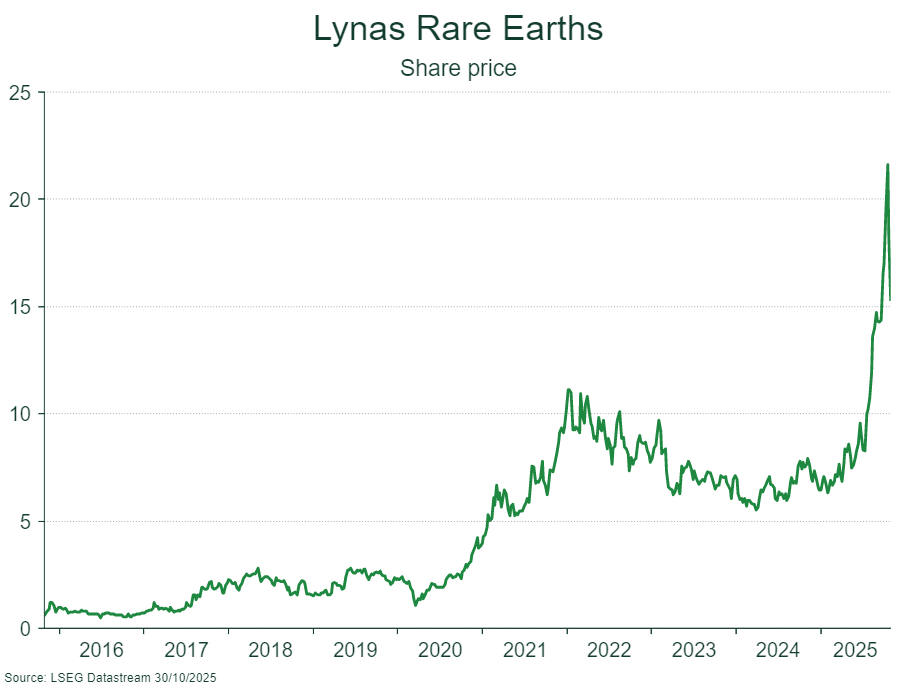

Faced with this assertive geopolitical manoeuvre, Western nations are pursuing strategic resilience in rare earths and a longer list of critical minerals. Australia has the world’s fourth-largest rare earth reserves, and is home to the only significant producer of heavy rare earths outside China, ASX-listed Lynas Rare Earths, which processes ore from Mt Weld in Western Australia at its Kalgoorlie facility as well as in Malaysia.

At their recent meeting in Washington, Donald Trump and Anthony Albanese announced a US-Australia critical minerals investment partnership, committing at least US$1 billion each towards an US$8.5 billion pipeline of joint mining and processing projects. Crucially, this collaboration includes setting a minimum price for critical minerals that guarantees stable revenue streams for new, high-cost Western processing plants and insulates them against the risk of future price dumping, which China historically used to eliminate competitors. This comprehensive US-Australia critical minerals investment strategy underscores the recognition that achieving supply chain sovereignty requires not only identifying new reserves, but also aggressively financing and defending the specialised processing capacity necessary to break the persistent 90% bottleneck currently held by China.

By Nick Ryder, Chief Investment Officer

Interest-Rate Outlook: Australia Steadies While the US Eases

After months of anticipation, investors on both sides of the Pacific are reassessing the outlook for interest rates. In the United States, the Federal Reserve has just delivered a widely expected rate cut, while in Australia, a stubborn inflation surprise has all but erased hopes of a Melbourne Cup Day cut. The divergence underscores two distinct economic stories: the Fed cautiously loosening to support growth, and the Reserve Bank of Australia (RBA) needing to pause amid renewed price pressures.

A Turning Point for the US?

In Washington this week, the Fed trimmed its benchmark federal funds rate by 25 basis points, acknowledging slowing growth and signs of cooling in the labour market. Chair Jerome Powell signalled that further reductions are possible but emphasised that the central bank’s data flow could be disrupted by the ongoing government shutdown. Markets now see the Fed near the end of its tightening cycle, with inflation trending closer to target and the focus shifting toward sustaining economic momentum.

The rate cut, though modest, reflects a cautious recalibration rather than a pivot. Powell’s message was clear: the Fed will proceed carefully, balancing the risk of doing too little to support activity against doing too much and reigniting inflation.

Australia: A Surprise Inflation Upswing

By contrast, Australia’s inflation data released this week painted a very different picture. The Australian Bureau of Statistics reported that underlying inflation rose to 3 per cent in the year to September, well above the consensus expectation of 2.7 per cent, and the first annual increase in three years. Headline inflation also ticked up to 3.2 per cent, driven by higher power bills, construction costs and persistent price rises in services such as travel, healthcare and veterinary care.

The trimmed-mean measure of inflation, the RBA’s preferred gauge, rose 1 per cent in the September quarter, significantly higher than the 0.6 per cent the Bank had forecast in August and even above Governor Michele Bullock’s earlier warning that a 0.9 per cent print would represent a “material miss.”

The reaction was swift. Futures markets slashed the implied probability of a Melbourne Cup Day cut from 80 per cent a week ago to less than 5 per cent. In a single morning, what had been framed as a celebratory Cup-Day easing has become a “late scratching,” as BetaShares chief economist David Bassanese put it.

Commonwealth Bank’s Belinda Allen said the data marked a clear turning point: “Given the material upside surprise to the CPI and the broad-based nature of pricing pressures, we now expect the RBA to remain on hold from here.” She added that if inflation stays high through 2026, “the RBA may need to act” with further hikes. Goldman Sachs’ Andrew Boak has withdrawn earlier forecasts for November and February cuts, arguing that the central bank will stay on hold “as it assesses the durability of the upside surprises to both inflation and the unemployment rate”.

Treasurer Jim Chalmers attempted to strike a reassuring tone, stressing that inflation at 3 per cent lies at the top end of the RBA’s target band and remains far below its 2022 peak. He attributed the jump largely to the expiry of state energy rebates, particularly in Queensland, Western Australia and Tasmania. Even so, many analysts regard the resurgence in services inflation, to 3.5 per cent from 3.3 per cent in the June quarter, as the most worrying element, signalling that the disinflationary trend has stalled.

The Outlook for the RBA

Taken together, the data and market response suggest the RBA’s easing cycle has ended, at least for now. After three 25 basis-point cuts earlier this year, the central bank appears content to wait and watch. Governor Bullock has consistently cautioned that wage growth and labour-market tightness pose upside risks, and the latest CPI print validates that concern.

While most forecasters still expect inflation to gradually cool through 2026, the path is likely to be uneven. Housing and energy costs remain volatile, and the winding back of government support measures is feeding directly into household budgets. For borrowers, this means rates are likely to stay higher for longer; for savers, deposit returns may remain appealing well into next year.

Global Divergence, Local Implications

The RBA is very unlikely to deliver a Melbourne Cup Day rate cut. Markets have now priced in a prolonged pause at 3.6 per cent, with some analysts even entertaining the prospect of hikes in mid-2026 if inflation fails to retreat.

In contrast, the US is easing, cautiously, as inflation cools and growth slows. For Australian households and investors, the message is one of patience and perspective: the disinflation journey is proving longer than hoped, but the RBA remains determined to anchor expectations and preserve financial stability as it guides the economy through this delicate phase.

Sources:

Reuters, The Australian Financial Review

Image Source:OpenAi

By Vincent O’Neill, CEO

Credit cockroaches

Wall Street is currently grappling with a warning issued by JPMorgan CEO Jamie Dimon regarding the surging private credit market. After a string of high-profile defaults and fraud allegations spooked investors, Dimon invoked a familiar metaphor to analysts on a recent earnings call: “When you see one cockroach, there are probably more. And so we should – everyone should be forewarned on this one”.

Dimon’s comments amplified existing concerns following US bankruptcies of car parts supplier First Brands Group and auto financier TriColor Holdings, which caused loan losses for lenders like JPMorgan and Jefferies. While executives at JPMorgan, Goldman Sachs, and Citi were quick to assure investors their private credit books were “diversified and high-grade”, Dimon was more cautious warning that additional risk will likely materialise when the next economic downturn arrives. “My antenna goes up when things like that happen,” Dimon noted, expressing suspicion about the credit underwriting standards of non-bank players in private credit.

The recent string of high-profile defaults strongly suggests that fraud and misrepresentation are the primary drivers of these losses, rather than purely operational failure. The failure of First Brands, which had borrowed over US$10 billion, was impacted by revelations over its extensive use of opaque off-balance-sheet asset backed finance and allegations that it pledged its accounts receivable to multiple lenders (i.e. it borrowed multiples times against the same invoices without lenders being aware). Similarly, subprime automobile financier and used-car dealer TriColor filed for liquidation with up to US$10 billion in liabilities after allegedly using duplicated vehicle identification numbers to generate multiple loans secured against the same physical vehicle. JPMorgan alone wrote off US$170 million in bad debt to TriColor.

Fraud allegations have also recently surfaced in real estate and private equity funds. Regional US banks like Zions Bancorp and Western Alliance recently disclosed bad loans tied to California commercial real estate investor Andrew Stupin and the Cantor Group. Lawsuits allege that funds tied to the Cantor Group misrepresented the collateral pledged against loans and, in one case, allegedly forged title insurance policies to obscure prior lending claims on the same properties. Stupin’s involvement is tied to around US$270 million in troubled debt.

Adding to the list of woes, the co-founder of private equity firm 777 Partners, Joshua Wander, was recently charged by the FBI over an alleged US$500 million fraud scheme. For reference 777 Partners was a lender to failed Australian airline, Bonza, which collapsed last year. At the core of the alleged fraud was the systematic practice of cheating lenders by “pledging assets that his firm did not own, falsifying bank statements, and making other material misrepresentations” about the firm’s financial condition.

Collectively, these events demonstrate that the real danger lies in the migration of risk from public credit markets and major banks into opaque corners of the financial system, specifically asset backed finance and private credit, where the lack of standardised, third-party oversight of collateral allows for excess leverage to accumulate and documentation fraud to flourish. The result is a game of pass the parcel in which lenders eventually discover that the same assets were promised to multiple creditors. Lenders are now racing to conduct forensic reviews of their loan portfolios, demanding stronger collateral verification, tighter documentation, and deeper due diligence to ensure they are not exposed to the next major credit collapse lurking beneath the surface.

While Dimon’s warning serves as a timely reminder of the risks lurking in the shadow banking sector, for now, the consensus among analysts holds that the foundation of asset backed finance and private credit remains resilient and the problems are not systematic, even if individual fraudsters have created significant temporary noise. The private credit funds we have approved have no exposure to any of these alleged frauds and in some cases deliberately avoided companies like First Brands because of numerous ‘red flags’ identified during their due diligence processes.

By Nick Ryder, Chief Investment Officer

Strategic Lifeline: Air T’s Acquisition of Rex and the Future of Regional Aviation

The protracted uncertainty surrounding Regional Express Holdings, better known as Rex Airlines, appears to be concluding with a strategic intervention from the US aviation services group, Air T. The North Carolina-based firm has entered into an agreement to acquire the distressed Australian carrier, a move that promises a critical capital injection and a potential restructuring of one of the country’s most politically sensitive transport assets. Announced in late October, the acquisition is expected to finalise before the year’s end, subject to standard court and regulatory approvals.

The sale marks a pivotal phase for Rex, whose recent history has been defined by overreach. The airline, historically celebrated as a reliable regional workhorse, took an ambitious and ultimately taxing gamble in 2021 by pushing into the hyper-competitive Sydney–Melbourne–Brisbane “golden triangle” routes. This direct confrontation with majors like Qantas and Virgin rapidly strained its balance sheet, coinciding with significant headwinds from rising global fuel costs and soaring aircraft maintenance expenses.

By mid-2024, the financial pressure became acute. The grounding of several ageing Saab 340 turboprops due to a lack of spare parts, coupled with mounting debts and the withdrawal of government support, forced the company into voluntary administration in August. This cash-flow crisis highlighted the high operational fragility of Australia’s smaller carriers.

Air T’s involvement offers more than just a purchase; it delivers deep sector expertise. The acquirer operates across aircraft leasing, parts supply, and logistics, possessing a strong track record of successfully integrating niche or distressed aviation businesses into its expansive platform. For Air T, Rex provides not only an established network of 50+ domestic routes but also invaluable infrastructure and regulatory reach within the Asia-Pacific market.

Crucially, the Australian Government underscored the systemic importance of the carrier by purchasing approximately $50 million of Rex’s debt. This action, as stated by Transport Minister Catherine King, was a calculated measure to preserve essential services for remote communities throughout the transition.

Air T has pledged to maintain Rex’s existing footprint, retain key senior management, and fund an essential engine-renewal program to modernise the regional fleet. While the purchase price remains undisclosed, this deal will be closely scrutinised by investors. It stands as a significant test of whether a specialised US strategic buyer can successfully extract long-term, sustainable value from a volatile, essential, and fiercely competitive Australian aviation asset. The outcome will likely redefine the commercial viability threshold for regional aviation in the country.

By Joey Mouracadeh, Senior Investment Director

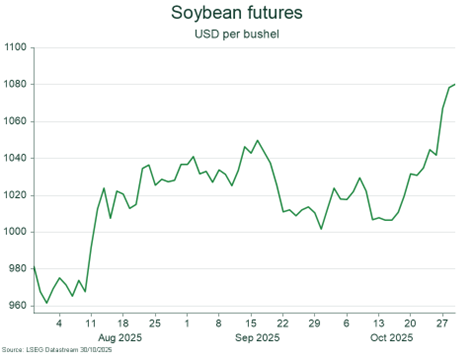

Soybean Rally Fuels Trader Profits Amid Global Shifts

Global soybean markets have experienced a period of significant turbulence over the past year, driven largely by shifting trade flows, geopolitical tensions, and evolving demand patterns from major importers. As one of the world’s most traded agricultural commodities, soybeans serve as a critical input for animal feed, food processing, and industrial applications, meaning their market movements are closely watched by farmers, exporters, and global investors alike.

The primary driver of recent volatility has been the ongoing US/China trade tensions. Restrictions on American soybean exports to China have redirected demand towards South American producers, particularly those in Brazil and Argentina. Brazilian and Argentinian farmers have expanded production to meet this growing demand, strengthening their global market positions and benefiting from higher global prices. Meanwhile, US producers face a more competitive landscape, grappling with lost market share, currency fluctuations, and elevated shipping risks. As a result, Soybean futures have emerged as a critical tool for navigating these market dynamics. Futures trading allows large scale agricultural businesses to manage risk and enables traders to potentially capitalise on price volatility. Recent months have seen substantial movements in futures contracts, reflecting both supply disruptions and speculation around geopolitical developments. For commodity traders, this volatility has translated into investment opportunities, which according to most reports have more often than not been profitable.

Taking a step back and zooming out, the broader economic implications of these market shifts are considerable. Price fluctuations in agricultural commodities can influence farming incomes, global food supply chains, feed costs, and country export revenues. In this case, countries that have increased production, such as Brazil and Argentina, are seeing positive economic impacts, while regions losing market share must contend with tighter margins and sectoral stress. It is important to note that this extends beyond soybeans as these trade and geopolitical shifts have also impacted other commodities, including the likes of Gold and Silver.

For investors, there are products readily available that take advantage of trading strategies that are seeking to exploit these market shifts. These are known as ‘trend following’ funds, which aim to detect and partake in the emergence of price trends across hundreds of markets around the globe. This is generally done through the use of a quantitative model which is specifically designed to capture asset price movements. Over the past twelve months, it’s likely that many of the top-performing trend-following funds have generated a significant portion of their returns from positions tied to agriculture and commodity markets as this focus has become increasingly prominent in global trade discussions.

By Joseph Nakhoul, Investment Research Analyst

Latest Podcast

SB Talks: Tariffs to Terabytes: – Trade Tensions, Tech Deals & the Gold Surge

In this episode of SB Talks, CEO Vincent O’Neill and CIO Nick Ryder, unpack the latest escalation in US-China trade tensions, focusing on China’s new rare earth export controls and their global ripple effects. They explore how these restrictions could impact industries from semiconductors to defense, and the strategic scramble for alternative suppliers.

The conversation shifts to OpenAI’s circular investment deals, with chipmakers like Nvidia and AMD raising questions about sustainability and bubble-like behaviour in the AI sector. Nick shares insights into the massive energy demands behind AI infrastructure and the uncertain path to profitability. The duo examines gold’s sharp rise, central bank buying, and the unusual coexistence of record highs in both equities and safe-haven assets.

Listen on Apple Podcasts

Watch on Youtube: