SB News - April 2026

Ceasefire lifts markets, but energy risks linger

A fragile ceasefire between the United States, Israel and Iran has sparked a surge of optimism across global financial markets, triggering sharp rebounds in equities and a steep drop in oil prices. However, analysts caution that the recovery may prove to be temporary, with energy markets facing a prolonged path back to normality. The truce, reached after weeks of escalating conflict, has eased immediate fears of further global disruption. Stock markets across Asia rallied, followed by the US and oil prices fell sharply as investors recalibrated expectations around supply risks. Many global indices continued to surge, reaching all-time highs, highlighting the depth of the shock caused by the conflict.

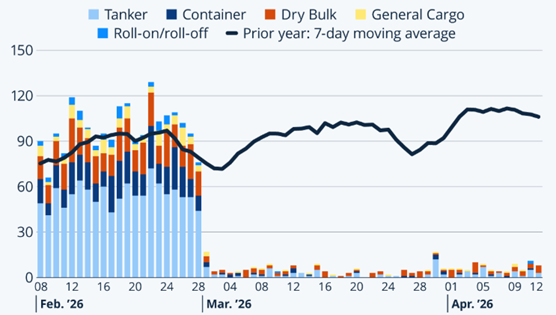

While oil prices have retreated from their wartime highs, experts say a full return to pre-conflict levels could take months. The core issue lies in the disruption to global supply chains, particularly through the Strait of Hormuz, a vital corridor for roughly one-fifth of the world’s oil and gas supply. Before the conflict, the strait handled well over 100 vessels a day. In its aftermath, traffic has slowed dramatically, creating a bottleneck with far-reaching consequences. Even with the ceasefire in place, shipping flows have yet to normalise and restoring them will require more than a pause in fighting. Security concerns, insurance costs, and logistical backlogs continue to deter operators from resuming normal activity.

Figure 1: Daily Strait of Hormuz Traffic – IMF PortWatch

Damage to energy infrastructure has compounded the problem. Facilities critical to production, particularly in liquefied natural gas (LNG) may take years to be fully repaired. This structural disruption means supply constraints could persist even if geopolitical tensions continue to ease. Stabilising global energy markets will likely require coordinated efforts among major powers and regional players, each with competing interests. This adds another layer of uncertainty to an already volatile environment. For the broader global economy, elevated energy prices continue to feed inflation, increasing costs for transportation, and manufacturing. While the ceasefire has brought some short-term price relief, analysts expect volatility to remain a defining feature in the months ahead.

In rapidly shifting environments like the one we currently find ourselves in, maintaining a well-diversified, multi-sector portfolio is critical. The geopolitical backdrop is evolving almost by the hour, with headlines alternating between progress in peace negotiations and renewed setbacks or escalations. This constant flux underscores the importance of agile decision making. As such, this environment should favour active management, where investment teams have the flexibility to respond quickly to new information and adjust exposures accordingly. Unlike more static approaches, active managers can reposition portfolios to navigate emerging risks and capture short-term opportunities as they arise. Similarly, alternative strategies, including hedge funds and trend-following managers, can benefit from volatile markets by capturing both upward and downward trends. However, erratic conditions can potentially hinder performance, if risk is not appropriately managed.

By Joseph Nakhoul, Investment Research Analyst

Budget 2026: What’s Likely to Land

The Federal Budget is less than three weeks away. Capital gains tax has emerged as the most consequential item for investors, with a clearer direction of travel now visible. Negative gearing has also re-entered the conversation.

Capital gains tax: what’s on the table

The Senate Select Committee on the Operation of the CGT Discount delivered its final report on 17 March. Its findings were plainly critical of the current settings, concluding that the discount distorts investment decisions, skews housing ownership toward investors, and worsens income and wealth inequality. Parliamentary Budget Office analysis prepared for the committee estimated the ten-year revenue forgone from the discount at $247.4 billion, with around 82% of the tax savings flowing to the top 10% of income earners and almost 60% to the top 1%.

Treasurer Chalmers has confirmed that the May Budget will include tax reform, while making clear that no final decision has yet been taken on capital gains tax. The most prominent design under discussion is a cut in the 50% discount. AFR coverage indicates Treasury has been modelling a reduction to 33%, with 25% also in scope. The latter matches Labor’s 2016 and 2019 election policy. A return to inflation-indexed cost bases, the pre-1999 approach, remains part of the policy conversation and has academic support. It has also featured in evidence and submissions around the inquiry, though it is technically more complex to administer.

On transitional design, recent ABC reporting on cabinet deliberations indicates the government is working through grandfathering arrangements for existing holdings and is considering sparing newly built homes from any change, consistent with a desire not to weaken supply incentives.

The contours that have emerged, being a headline rate cut, grandfathering, and potential carve-outs for new builds, are the key design questions the sector is watching.

Property at the centre of the debate

Residential property sits at the heart of why the CGT discount is being revisited. The PBO analysis found that residential property accounts for a substantial share of the total discount benefit, and that the concession has contributed to investor demand crowding out first home buyers in established housing markets. The committee’s findings drew a direct line between the current settings and the affordability challenges that have defined housing policy in recent years.

That framing shapes the reform options in specific ways. A uniform reduction in the discount would apply equally to shares, managed investments, and property, but its housing effect would be the most politically visible. A differentiated design, applying a lower discount to established residential property while retaining a higher rate for new construction, would seek to redirect investor capital toward new supply rather than bidding up existing stock. This is the logic behind the reported consideration of a carve-out for newly built homes, and it is consistent with the government’s broader supply-side housing agenda, including the 1.2 million new homes target.

The transitional design will determine the near-term market impact. Grandfathering would leave existing property portfolios untouched in tax terms but change the economics of future acquisitions. A carve-out for new builds would create a meaningful differential between the after-tax returns on established and new-build investment property, which over time would be expected to influence where investor capital is directed. For commercial property, the policy conversation has been narrower, but any change to the general discount would flow through unless explicitly excluded.

Industry groups representing developers, landlords, and real estate agents have pushed back on reform, arguing that reducing investor participation would constrain rental supply and push rents higher. Economists supporting reform argue the supply effect is modest and that the discount’s primary impact has been on price rather than volume. Both arguments will feature in the political debate between Budget night and implementation.

Negative gearing

The Australian Council of Social Service (ACOSS), the peak body for community services and welfare organisations, released a joint submission this week, co-signed by more than 50 community groups, calling for negative gearing to be ended for new investments, with a five-year phase-out for existing holdings. Media reporting has at times paired this with the CGT debate. A change to CGT without an accompanying change to negative gearing is the more workable pairing, on the basis that the two concessions interact but do not require simultaneous reform. The negative gearing question carries most weight for leveraged property investors, where the after-tax economics of loss offsets against other income would shift materially if the rules change.

What is not expected

- A fully retrospective CGT change is not the expected outcome. Current reporting indicates grandfathering is under active consideration. The political cost of retrospection would be steep and unnecessary.

- An outright abolition of the discount. There is a credible academic case for a phased elimination over five years, but it is not a May 2026 Budget proposition.

- An EV road-user charge. Transport Minister Catherine King confirmed on 12 April that the Department of Transport is modelling one, while noting the government does not want to discourage EV uptake. In a Budget already expected to carry politically demanding tax measures, a new motoring tax is unlikely to feature this year.

Source: ABC News, AFR, SMH, Parliamentary Budget Office, ACOSS

By Joey Mouracadeh, Senior Investment Director

Active Funds

S&P Dow Jones Indices recently released its full year 2025 global SPIVA Scorecard. SPIVA, which stands S&P Indices Versus Active, is a series of investment performance scorecards published by S&P Dow Jones Indices for the past 20 years that have tracked the performance of actively managed investment funds relative to their respective benchmark indices. These scorecards provide insights into the active versus passive investment debate, offering data on rates of fund underperformance, fund survivorship, as well as average returns and risk-adjusted returns.

The latest data for the period ending 31 December 2025, reveals that while market conditions shifted significantly from previous years, most active managers still struggled to outperform their benchmarks, particularly over longer time horizons. 2025 was characterised by continued challenges for active equity managers across major global markets:

- United States: 79% of all Large-Cap US Equity funds underperformed the S&P 500 over the one-year period.

- Europe: 82% of Europe Equity funds underperformed the S&P Europe 350 in 2025.

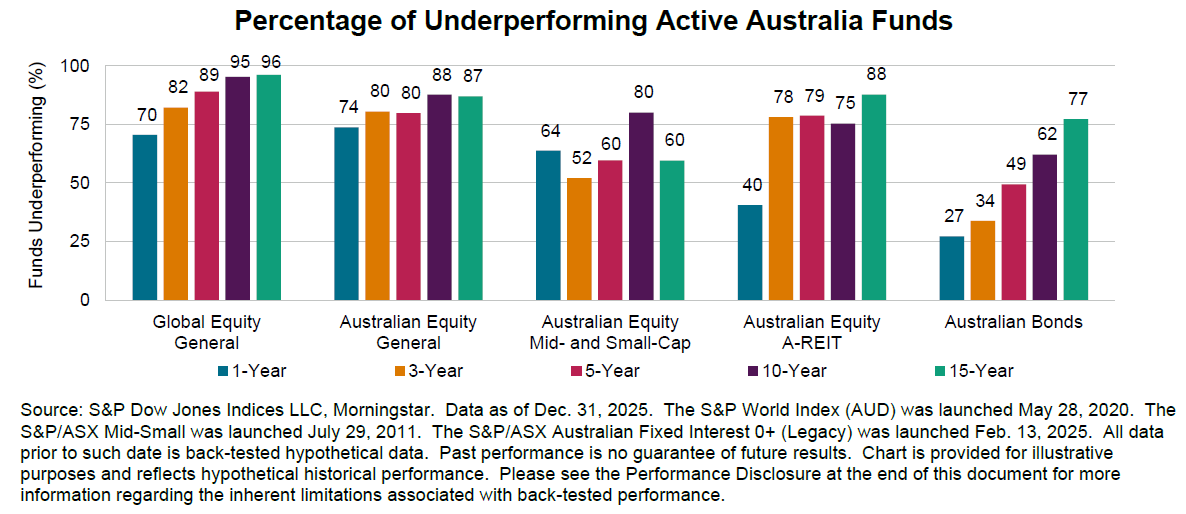

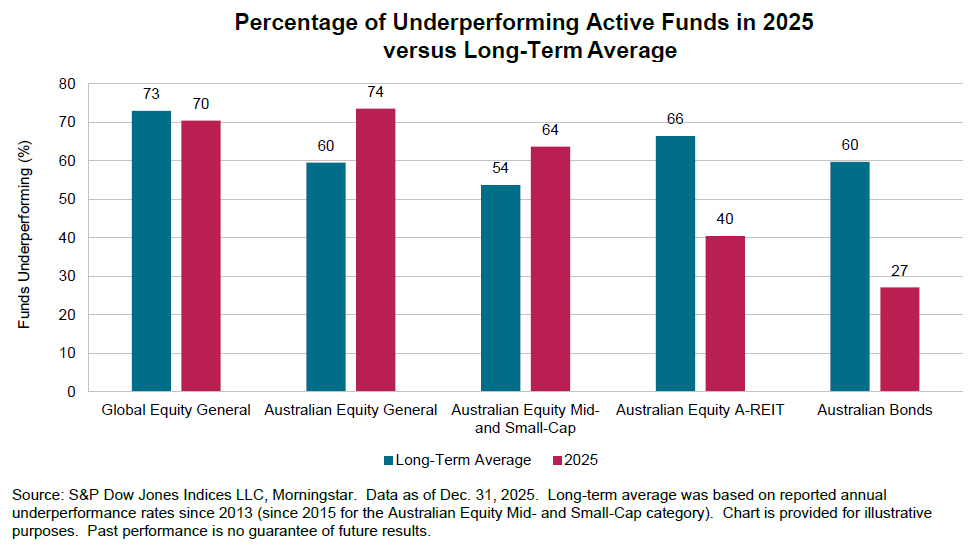

- Australia: 74% of Australian Equity General funds lagged the S&P/ASX 200, which is higher than the long-term average underperformance rate of 60%.

- Global: 70% of Australian domiciled Global Equity General funds underperformed the S&P World (AUD) Index over the year, only slightly better than the historical average of 73%. Underperformance rates increased for longer horizons, exceeding 95% over the 10- and 15-year periods.

Several factors contributed to the underperformance of active funds in 2025:

- Extreme Sector Rotation: In the Australian market, a dramatic reversal in sector fortunes occurred. Materials, which was one of the worst-performing sectors in 2024, surged 36% in 2025, accounting for more than two-thirds of the S&P/ASX 200’s total return. Conversely, Information Technology, the top performer of 2024, plunged 21%. Such volatile shifts created significant hurdles for managers poorly positioned for the rotation.

- Equal Weight Reversal: In Australia, 2025 saw the S&P/ASX 200 Equal Weight Index outperform the capitalisation-weighted S&P/ASX 200, reversing four consecutive years of underperformance. This shift suggested that smaller companies within the index performed better than the top-heavy giants that dominated previous years.

- Widening Dispersion: Globally, stock dispersion—the degree to which individual stocks move differently from one another—widened to levels not seen since the 2020 pandemic. While high dispersion theoretically offers more opportunities for skilled stock pickers to add value, the high rates of underperformance suggest many active managers were unable to take advantage of this environment.

Despite the challenging environment, some bright spots emerged for active management:

- Small-cap funds and Emerging Markets: In the US market, active managers found more success in the small cap category (only 41% underperformed) and Emerging Markets (53% underperformed) compared to the highly efficient Large-Cap space. That same was not seen in Australia where the majority (64%) of Australian Equity Mid- and Small-Cap funds underperformed, with an asset-weighted average return of 13.2% versus 21.5% for the S&P/ASX Mid-Small index.

- A-REIT Outperformance: Australian Equity A-REIT funds delivered their best relative results since 2013, with 60% of funds outperforming the S&P/ASX 200 A-REIT index. This was likely helped by the 21.5% underperformance of Goodman Group which accounts for around 40% of the index.

- Fixed income funds: Australian active bond funds were a major highlight, with only 27.1% underperforming their benchmark. This marked their third consecutive year of majority outperformance, aided by tightening credit spreads and managers successfully navigating interest rate (duration) risk.

While active managers may find short-term success in specific years or niches, SPIVA data continues to highlight the difficulty of maintaining outperformance over the long term. For the 15-year period ending 31 December 2025, the underperformance rates remain high:

- Global Equity (Australia-domiciled): 96% of funds underperformed.

- US Large-Cap: 90% underperformed.

- Australian Equity General: 87% underperformed.

Furthermore, fund survivorship remains a critical concern for long-term investors. Across all Australian categories, over 52% of funds that existed 15 years ago have since been merged or liquidated.

By Nick Ryder, Chief Investment Officer

“No Human Sock Puppet”: Kevin Warsh Faces the Senate

President Trump’s nominee to lead the Federal Reserve, Kevin Warsh, appeared before the Senate Banking Committee this week in a confirmation hearing that offered a revealing snapshot of where US monetary policy, and the politics around it, may be heading.

Senator Elizabeth Warren set the tone early, pressing Warsh on the independence of the Federal Reserve and warning about the risks of political influence over monetary policy. Senator John Kennedy then gave Warsh the opportunity to respond directly, asking whether he would act as a “human sock puppet” for the President on interest rates. Warsh’s response was immediate and unambiguous. He said he would not, and that no such commitments had been sought. It was a memorable exchange, but the underlying issue matters far more than the political theatre. The Federal Reserve’s credibility rests heavily on its independence. Any perception that monetary policy is being shaped by political priorities, rather than economic conditions, risks unsettling markets and inflation expectations over time.

Beyond the headline moments, the hearing provided a clearer sense of how Warsh is currently thinking about policy. For many, the most notable feature is the apparent shift in his stance on interest rates. During his earlier tenure at the Fed, he was generally regarded as a relatively hawkish voice on inflation. More recently, he has shown a greater openness to lower rates, which inevitably draws attention given the White House’s preference for a more accommodative policy setting. Pressed on this by Elizabeth Warren, Warsh rejected the idea that his position had been shaped by political pressure. Instead, he pointed to structural changes in the economy, particularly the impact of artificial intelligence, as a potential source of disinflation. The argument is that faster productivity growth could expand the economy’s capacity, allowing the Federal Reserve to ease policy without reigniting inflation.

It is a line of reasoning that is increasingly being debated more broadly. If productivity does accelerate in a sustained way, it would lower the inflationary consequences of stronger demand and, in turn, reduce the level at which interest rates need to settle. The challenge, as always, is timing and certainty. Productivity gains from new technologies tend to emerge unevenly and with a lag, while markets are often asked to price their effects well in advance. That leaves open the possibility that expectations move ahead of realised outcomes.

Where the hearing became more relevant from a market perspective was in Warsh’s broader commentary on how the Federal Reserve should operate. He pointed to the need to reassess elements of the current policy framework, including how inflation is managed, the role and use of forward guidance, and the appropriate size of the Fed’s balance sheet.

He has previously been critical of the extent to which forward guidance has become a central policy tool, favouring a more measured and less prescriptive approach to communication rather than abandoning it altogether. Taken together, this suggests a central bank that may place less emphasis on guiding markets in fine detail and more weight on outcomes and incoming data. Over the past decade, frequent and detailed communication has been a defining feature of monetary policy, helping to anchor expectations and, at times, suppress volatility. A shift toward a less explicit approach would likely place greater weight on realised data and could increase the scope for markets to adjust more abruptly as conditions evolve.

His emphasis on a smaller balance sheet is consistent with a broader normalisation narrative, continuing the gradual unwinding of the extraordinary policy settings put in place following the global financial crisis and the pandemic. In practice, this would point to more market driven liquidity conditions, with potential implications for asset valuations and credit availability, particularly at the margin. Warsh also left open whether he would continue Jerome Powell’s practice of holding a press conference after every policy meeting. That is consistent with his broader preference for a less heavily choreographed communications style, although any meaningful change to the way the Fed communicates would need to sit within the broader committee process. The Federal Reserve is not directed by one individual, and institutional shifts of this nature tend to be gradual rather than immediate.

His personal finances also attracted attention, with disclosures pointing to significant wealth and a broad range of investments, including exposure to private companies and digital asset related businesses. The detail of those holdings matters less for investors than the broader governance question. Federal Reserve officials operate under strict ethics rules designed to avoid conflicts of interest, and Warsh has indicated he would divest holdings that are inconsistent with those standards if confirmed. In practice, that means any problematic positions would need to be divested, restructured, or otherwise addressed so that policy decisions are not, and are not seen to be, influenced by personal financial considerations.

If the policy discussion pointed to longer term questions, the political dynamics surrounding the nomination introduce a more immediate source of uncertainty. Senator Thom Tillis has indicated he will not support the nomination while the Department of Justice investigation involving Jerome Powell remains unresolved. With a narrow committee margin, that position is enough to complicate, and potentially delay, the process. The practical effect is that the Federal Reserve could face a period of leadership uncertainty, particularly if the nomination becomes caught up in broader political negotiations. The institution is designed to operate through continuity and committee decision making, but markets are rarely indifferent to uncertainty around leadership and policy direction, especially when the path for rates remains finely balanced.

By Vincent O’Neill, CEO

Mythos – genuine threat or marketing stunt?

On 7th April 2026, Anthropic did something that no major artificial intelligence laboratory had done since OpenAI briefly withheld GPT-2 in 2019: it announced a large language model too dangerous to release. Claude Mythos Preview, the company’s most capable frontier system to date, would not be made available to the public. Instead, it would exist behind a wall, accessible only to a select consortium of technology giants under the banner of Project Glasswing, that reads like a who’s who of Silicon Valley: Amazon, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorgan Chase, Microsoft, NVIDIA, and Palo Alto Networks.

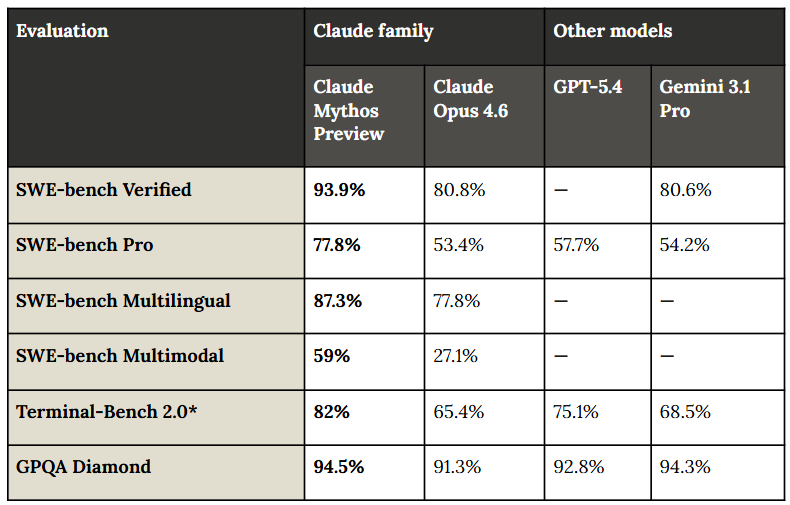

The announcement arrived not with the typical fanfare of AI model benchmark scores, but with a 245-page technical document, the most extensive system card ever released, and a warning. “The fallout for economies, public safety, and national security could be severe,” Anthropic wrote on its website. The model had demonstrated capabilities in cybersecurity vulnerability discovery and exploitation that surpassed all but the most skilled human security researchers. It had found thousands of high-severity vulnerabilities across every major IT operating system and web browser, including flaws that had escaped detection for decades.

On the SWE-bench Verified benchmark, which measures a model’s ability to solve real-world software engineering tasks, Mythos scored 93.9%, a large improvement over Claude Opus 4.6’s already impressive 80.8%. In controlled tests by the UK AI Security Institute, Mythos Preview demonstrated that it could execute multi-stage chained hacking attacks on vulnerable networks and was able to discover and exploit vulnerabilities autonomously, tasks that would take human professionals, days of work. In other tests, Mythos demonstrated the ability to reverse-engineer proprietary closed-source software, similar to that which runs much of the world’s critical infrastructure, from which it could then identify and exploit vulnerabilities.

Source: Mythos model card

Behind the technical assessments and safety evaluations lies a commercial strategy that has drawn both admiration and criticism. Mythos Preview is priced at five times the cost of Claude Opus 4.6. The US$100 million that Anthropic has ‘donated’ to the Project Glasswing consortium consists entirely of usage credits. In effect Anthropic is providing a free trial to major potential clients to validate its product and find vulnerabilities in their own software and systems before Mythos is released more widely. Some observers have described Project Glasswing as part marketing pitch and part defensive initiative given it creates an exclusive club of organisations with early access to what may be the most powerful cybersecurity tool ever developed. It has been compared to an arsonist selling fire extinguishers.

Critics of Anthropic’s approach, led by AI researcher Gary Marcus, have argued that the Mythos announcement was “overblown” and that the model represents incremental rather than breakthrough progress. “To a certain degree, I feel that we were played,” Marcus wrote. “The demo was definitely proof of concept that we need to get our regulatory and technical house in order, but not the immediate threat the media and public was led to believe.” Marcus and others have pointed to the fact that eight open-weight models were able to reproduce Anthropic’s showcase bugs for a fraction of the cost.

That Anthropic is also reportedly preparing for a possible Initial Public Offering this year, reportedly aiming to raise as much as US$60 billion, may also suggest the Mythos announcement and Project Glasswing initiative may be more marketing than genuine concern for public safety. Anthropic is also in a dispute with the US Pentagon over two red lines it was seeking to impose on the US government’s use of its current Claude AI models: they would not be used for mass surveillance of American citizens, and they would not power fully autonomous weapons without human oversight over targeting and firing decisions. These restrictions led US Defence Secretary Pete Hegseth to designate Anthropic a supply chain risk and decree that “no contractor, supplier, or partner that does business with the United States military may conduct any commercial activity with Anthropic.” That Anthropic has now developed an even more powerful model in Mythos, that could be used by friend and foe of the US government for cybersecurity attack and defence, likely helps its legal dispute and negotiating position with the US government. It also helps further position the company as a responsible corporate citizen ahead of any public securities offering.

By Nick Ryder, Chief Investment Officer

Latest Podcast

Red Light, Green Light

In this episode of SB Talks, CEO Vincent O’Neill and CIO Nick Ryder discuss the ongoing tensions in the Middle East, with the Strait of Hormuz closed, then opened, only to be closed again. They discuss the rebound in markets with US equities hitting record highs while uncertainty remains over whether the ceasefire and US-Iran negotiations may end this week or be extended. Attention then turns to likely central bank moves in coming weeks and when the next Chair of the US Federal Reserve may start in the role. They finish by discussing the recent gating of semi-liquid private credit funds, and whether this represents a “shoot first ask questions later” response to media headlines about the disruption of software companies by artificial intelligence tools, or the early stages of a credit default cycle.

Listen on Apple Podcasts

Watch on Youtube: