SB News - August 2025

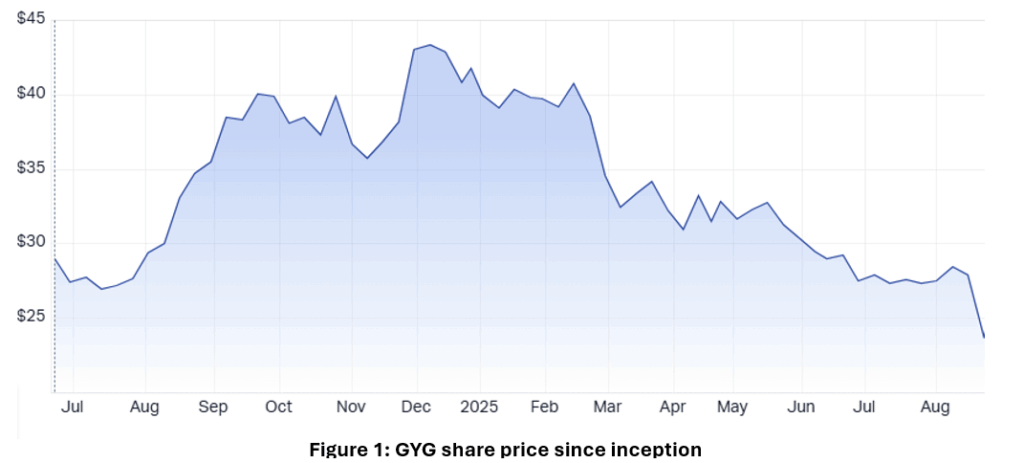

Reality Bites for Guzman y Gomez Founder as Shares Tumble

The honeymoon period is over for Steven Marks and his fast-growing burrito empire, Guzman y Gomez (GYG). Just over a year after its blockbuster IPO on the Australian Securities Exchange made headlines making Marks a multimillionaire, the Mexican-themed fast-food chain is confronting a harsh dose of investor reality. GYG shares plunged 18% on Friday the 22nd of August, the steepest drop since its listing, after the company reported slower than expected sales growth in its core Australian market. The selloff wiped more than A$160 million from Marks’ fortune, cutting the value of his stake to around A$235 million, down more than 40% from its peak in February 2025. Earlier this year, the company revealed margin pressure at the restaurant level, and August’s earnings call did little to allay concerns. The sharp downturn underscores growing investor unease over the company’s performance and its ambitious growth strategies.

Founded in 2006, Guzman y Gomez was born out of Marks’ frustration with what he saw as a lack of authentic Mexican food in Australia. A former Wall Street trader with stints at SAC Capital and Cheyne Capital, Marks left finance to pursue something radically different by bringing fast, fresh, and flavourful Mexican cuisine to a market dominated by traditional fast-food giants. Named after two of his Mexican friends, the brand quickly built a loyal following, standing out for its use of clean ingredients, no added preservatives, and a health-first approach to fast food. From a single store in Sydney, GYG has grown into a national sensation with stores in over 200 locations and plans to open 1,000 restaurants across Australia — a scale that would rival McDonald’s.

For many, the excitement of Guzman y Gomez’s public listing would have been driven by brand familiarity and a genuine love for Mexican cuisine. This connection most likely contributed to the stock’s strong early momentum, with its price surging in the first eight months post-listing. The IPO saw strong retail demand with some sources suggesting that scale-backs of up to 90% were being applied to applications. This would mean an investor applying for $100,000 worth of shares may be allocated only $10,000 worth of stock. However, when it comes to investments such as this, it is important to remain mindful of behavioural biases that arise and to avoid making investment decisions that are fuelled by them. To reduce this risk an appropriate course of action is to invest with experienced Australian equity managers, who have deep expertise, strong industry networks, and access to rigorous company analysis. Some of these managers may even be able to participate in IPOs, and for GYG this was the case. Certain fund managers were invited to participate in the IPO but declined after conducting thorough due diligence and determining that it was not a viable investment to make. At the time of the IPO there was even light-hearted commentary amongst fund managers speculating on how far the stock might run, aware of the bullish sentiment from retail investors. In the end, discipline prevails, as earnings and profitability continue to remain the true drivers of long-term share price performance.

By Joseph Nakhoul, Investment Research Analyst

BlackRock Setback Highlights Challenges in Private Credit

Private credit markets, once the darling of alternative investments, are showing signs of growing pain, where even finance industry giants are not immune. BlackRock, the world’s largest asset manager, recently paused fundraising for its latest Asia-Pacific private credit fund, illustrating how even trillion-dollar institutions face hurdles in this increasingly competitive and crowded space. The pause, which came after BlackRock’s December 2024 announcement to acquire HPS Investment Partners, reflects both internal transition and external market challenges. While the acquisition of HPS was designed to bolster BlackRock’s private markets presence, it temporarily sidelined efforts to raise the firm’s third Asia-Pacific private credit fund. The original fund raising target was US$1 billion, a figure that was later proven to be too ambitious to reach.

This development follows a series of setbacks for the group as key investor Arch Capital is reportedly looking to divest at least US$350 million of funds, citing disappointing performance and high executive turnover. In parallel, BlackRock and Mubadala Investments, Abu Dhabi’s state-backed fund, mutually dissolved their private credit partnership after struggling to source attractive deals in the current environment. These events point to a broader issue affecting the global US$1.7 trillion private credit market, which is too much capital chasing too fewer quality deals’.

For investors, the key challenge becomes how to navigate a saturated market where newer entrants, regardless of size, may struggle to build credibility and secure consistent deal flow. Strategically aligning with established incumbent managers, with deep experience, proven strategies, and resilient track records across economic cycles could potentially be the answer. In uncertain markets like the one we currently found ourselves in, experience matters more than ever. Well-known asset managers such as Metrics, Ares and Churchill have deep-rooted networks that drive steady deal flow that are often sourced from existing relationships where speed, trust, and execution are valued over marginal pricing advantages offered by lesser known competitors.

While BlackRock is globally respected, its private credit platform is not its prime focus, and borrowers remain more comfortable with seasoned lenders like the three mentioned above, managers that Stanford Brown has aligned with. These institutions are known for their ability to deploy capital efficiently and maintain disciplined underwriting standards, even in frothy or volatile market conditions. As a collective group they offer investors diversified access to both domestic and global opportunities. They provide credit strategies focused on large companies as well as mid-market businesses. By operating in distinct market segments it means that these managers will very rarely compete against each other on the same lending deals. This segmentation enhances deal diversification and reduces the overall risk of portfolio stagnation for clients.

By Joseph Nakhoul, Investment Research Analyst

The Federal Reserve Under Pressure

The independence of the United States Federal Reserve is facing one of its most serious challenges in recent memory. This week, President Donald Trump announced that he had dismissed Federal Reserve Governor Lisa Cook, citing allegations of mortgage fraud. Cook has strongly denied the allegations, making clear that a President has no authority to dismiss a sitting Governor. She has initiated a process to contest the move in the courts.

This is not an isolated incident. It follows a broader pattern of political pressure on the central bank. During this term, Trump has repeatedly criticised Federal Reserve Chair Jerome Powell, whom he himself appointed during his first term, for not cutting interest rates fast enough. He even suggested he had the authority to demote or remove Powell. Those claims were never acted upon, but they set a precedent for open confrontation between the White House and the Fed. The attempted removal of Cook represents an escalation, turning rhetoric into action.

Why central bank independence is essential

Central banks exist to take a long-term, steady view of monetary policy. They are designed to resist the pull of short-term political cycles and instead focus on sustainable growth, employment stability, and inflation control. The United States Federal Reserve is particularly important, given its role in setting the tone for global financial conditions.

Federal Reserve Governors serve 14-year terms and can only be removed “for cause.” This safeguard is intended to ensure that Governors cannot be dismissed simply for holding views that differ from a political leader. Without this protection, the temptation for governments to push for artificially low interest rates to stimulate short-term growth before an election would be overwhelming. The result could be higher inflation, reduced productivity, and diminished long-term economic prosperity.

The wider economic backdrop

This dispute comes at a delicate moment. Inflation, while easing, remains a challenge in many economies. Productivity growth, particularly in advanced economies, has been uneven. At the same time, investment in new technologies, infrastructure, and new energy is essential to sustain long-term competitiveness. For all these reasons, confidence in the Fed matters.

If investors believe that the Federal Reserve is losing independence, the effects can flow quickly through markets:

- Bond markets may see yields rise as investors demand compensation for higher inflation risk. This raises borrowing costs for households, businesses, and governments.

- Currency markets may see pressure on the US dollar, which could alter trade balances and investment flows worldwide.

- Equity markets could experience volatility. While some sectors may welcome lower interest rates, uncertainty generally discourages the kind of long-term capital deployment that supports sustainable growth.

History shows that when political leaders openly challenge central banks, the damage is not just immediate market turbulence. It can also erode the credibility of institutions that anchor long-term economic stability.

At the heart of this issue is more than a debate about personalities or power. Sustained economic prosperity requires steady inflation, predictable interest rates, and strong institutional credibility.

For investors, the key is not to react to headlines with panic, but to recognise the importance of diversification and discipline. A resilient portfolio does not rely on the assumption that waters will always be calm. Instead, it is built with the understanding that economic shocks, political disputes, and legal battles are sometimes, unfortunately, a natural part of the landscape.

By Vincent O’Neill, CEO

The Shadow AI Economy

In recent weeks, headlines have circulated that artificial intelligence is stalling in business. One widely cited figure from MIT (Massachusetts Institute of Technology) suggests that 95% of enterprise generative AI pilots fail to produce material gains. At first glance, this sounds like proof that the technology is overhyped. In reality, research shows something more nuanced. AI is not failing. It is succeeding in unexpected places, particularly in what has been called the “shadow AI economy.”

Enterprise Pilots Versus Real-World Use

MIT’s NANDA initiative, which examined over 300 AI deployments and surveyed 350 business leaders, found that corporate pilots are indeed struggling. Around USD 30 to 40 billion has been invested in generative AI by enterprises, but only about 5% of pilots have delivered rapid gains. The main reasons are flawed integration, lack of learning capabilities, and tools designed without considering how employees actually work.

Yet beneath these disappointing pilot statistics lies another truth. More than 90% of employees report using generative AI tools such as ChatGPT, Claude or Gemini in their everyday roles. In other words, employees are bypassing official systems and adopting consumer AI products themselves, creating a hidden layer of productivity growth.

Hard Data on Productivity Gains

The evidence for real productivity improvements is still emerging. A GitHub Copilot (Peer-Reviewed Study) review of Copilot use in real projects reported up to 50% less time spent on documentation and autocomplete, and 30 to 40% reductions in repetitive coding, debugging and unit test generation. Another evaluation reported by Cornell University covering nearly 400 developers recorded a 33% suggestion acceptance rate, with 72% reporting high satisfaction. Together, these studies confirm that general-purpose AI tools are already delivering replicable time savings and quality improvements.

Economic and Market Implications

When scaled across millions of workers, even modest time savings translate into meaningful output. If knowledge workers save 20 to 40% of their time on routine tasks, they can redirect effort into higher-value work. Economists often compare AI to electricity or the internet technologies that initially disappointed but later transformed productivity once widely embedded.

Forecasts vary, but the scale of potential is clear. McKinsey estimates that generative AI could add USD $2.6 to $4.4 trillion annually to global GDP, representing 15 to 40% of the total economic impact of all AI applications (mckinsey.com). The European Central Bank has modelled scenarios where a sectoral productivity gain of 11% could lift aggregate GDP by 7% over a decade.

For investors, this matters. Official adoption metrics that emphasise enterprise pilot failures risk understating the productivity wave already building beneath the surface.

Looking Ahead

The message is clear. AI is not failing. It is working where people find it useful, accessible and adaptive. The challenge for organisations is to recognise this reality and support the tools that employees value. The challenge for policymakers and economists is to capture these hidden productivity gains in official statistics. And the challenge for investors is to look beyond the headlines of failure and identify the firms quietly driving efficiency and growth.

By Vincent O’Neill, CEO

Sources: www.fortune.com, McKinsey, Cornell University

July’s Inflation Jolt and the Deeper Questions for Productivity and Markets

Australia’s inflation rate jumped to 2.8% (year on year) in July, up from 1.9% in June, driven largely by a 13% surge in electricity costs following the expiry of temporary federal and state rebates.

The Reserve Bank of Australia (RBA) targets inflation midway between 2 and 3%. On that basis, July’s figure marks a significant move in the wrong direction. But as most economists note, the spike is not evidence of broad-based inflationary momentum. Instead, it reflects the end of subsidies that had artificially suppressed household energy bills. With a scaled-back rebate now in place, the impact should moderate in coming months.

This helps explain why expectations for another rate cut later this year remain intact. The RBA places more weight on quarterly measures of underlying inflation, which strip out temporary distortions. That said, the July print is a reminder that one-off policy choices can feed into headline inflation in ways that unsettle both households and markets.

For borrowers, recent rate cuts have already delivered welcome relief. Some households are spending the surplus, boosting consumer demand. Others are keeping repayments steady, accelerating debt reduction, and insulating themselves against future shocks. Both choices matter. Higher consumption supports business turnover, while faster debt repayment strengthens household balance sheets and reduces systemic risk.

The Productivity Challenge

Beneath the inflation headlines lies a more stubborn issue: Australia’s weak productivity growth. For the past decade, labour productivity has stagnated, with output per hour worked falling in several recent quarters. This is not just an academic concern. Productivity is the foundation of long-term living standards, competitiveness, and sustainable wage growth.

Government initiatives, from the Future Made in Australia Act to investments in energy transition and skills, aim to lift national capability. Yet scepticism is warranted. Subsidies for critical minerals, renewable energy, and advanced manufacturing may create jobs and stimulate investment, but they do not guarantee higher productivity.

Implications for Investment Markets

For investors, the interplay between inflation, rates, and productivity is central. If the July surge proves temporary, and if the RBA resumes cutting rates, the backdrop is supportive for equities, property, and infrastructure. Lower borrowing costs reduce hurdle rates for projects, encourage capital deployment, and underpin consumer confidence.

However, without stronger productivity growth, the economy risks sliding into a cycle of weak output, higher unit labour costs, and recurring inflationary flare-ups. This would undermine the very conditions investors rely on for stable returns. A low-rate environment can be positive for valuations in the short term, but long-term market performance depends on whether Australia can lift its productivity trajectory.

A Cautious Outlook

The July inflation figure is a useful reminder that the path back to price stability is fragile, and that policy interventions often mask rather than solve underlying pressures. Borrowers are enjoying breathing room, but the sustainability of that relief depends on productivity improvements that have so far been elusive. Government initiatives hold promise, but their effectiveness is not yet proven.

In short, the near-term outlook for borrowers and investors remains constructive, with further rate cuts likely. But the longer-term question is whether Australia can escape its productivity malaise.

By Vincent O’Neill, CEO

Investor Confidence Reignites New York’s Office Market Amid Signs of Recovery

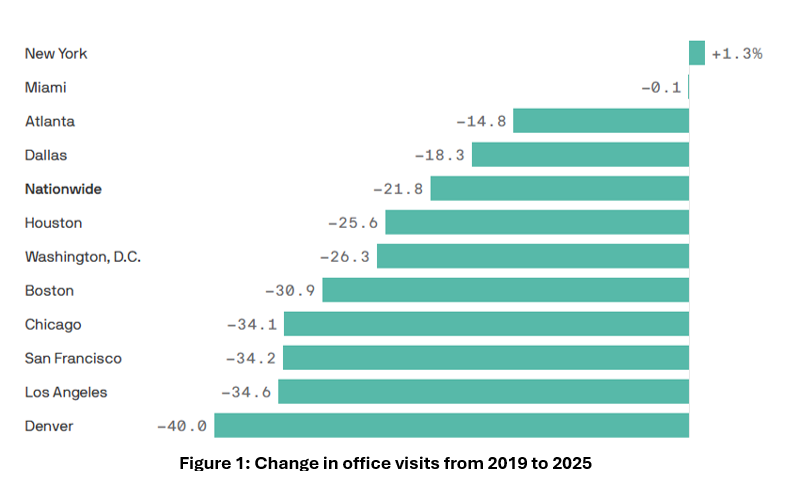

A renewed wave of investor interest is revitalising New York City’s commercial real estate sector, signalling a potential turning point for the office market after years of economic uncertainty. In 2025, developers have already raised more than US$11 billion through commercial mortgage-backed securities (CMBS) underpinned by New York office properties. This is the highest level since before the Federal Reserve began hiking interest rates in 2022. The resurgence is being driven by refinancing activity in prominent, well-leased office towers. Four major skyscrapers alone have secured a combined US$3 billion in CMBS financing this year, highlighting a return of confidence in the stability and long-term viability of office assets, particularly those in prime locations. Many attribute the recovery to a steady uptick in return-to-office mandates from major corporations. This shift is particularly visible along central business districts which are known for their large concentration of legal and financial firms, where leasing and foot traffic have also both increased notably in recent months. As a matter of fact as of July 2025, office foot traffic in New York surpassed its pre-pandemic levels for the first time, registering a 1.3% increase compared to July 2019.

This renewed activity represents a sharp contrast to the shaky market environment that defined 2023 and 2024. In fact, based off recent data, office availability in Midtown Manhattan has dropped from 18.2% to 15.5% year-over-year, a clear sign that the leasing environment is strengthening. Complementing this trend, New York City subway usage has climbed back to 72% of its pre-pandemic levels, suggesting a broader return to weekday commuting. Institutional investors are also beginning to take notice with private markets giant KKR investing approximately US$400 million in office backed CMBS this year, pointing to stabilising fundamentals and an improving vacancy picture. Many see these indicators as evidence that the office market may have reached or is nearing its bottom. With the vast majority of financing going to well-leased properties with strong tenant rosters in central locations, some concerns however continue to remain for outdated office buildings.

In a fragmented market such as this, it is vital to align with large institutions, such as KKR and Nuveen, who due to their extensive real estate platforms, are well-positioned to take advantage of rapid market changes that may occur. These large asset managers generally have a physical presence in prime city locations across the world, such as New York, and as a result are able to remain on top of any new regulatory or economic developments that occur, potentially allowing them to move quicker than competitors operating out of one central location. Large asset managers are also more likely to be able to invest in prime office buildings as they have the scale and size to do so. Despite all of the positivity surrounding the office sector, it is important to note that for now, most institutional portfolios continue to carry minimal exposure to it, and any exposure that there might be is generally locked up in prime assets. However, as these buildings become fully leased, the focus may begin to shift towards well-located lower tier assets, potentially opening a new chapter for office sector investing in the foreseeable future.

By Joseph Nakhoul, Investment Research Analyst

Latest Podcast

SB Talks: Rates Revisions and Revolving Doors

In this episode of SB Talks, CEO Vincent O’Neill and CIO Nick Ryder, unpack the latest US jobs shock, where a massive downward revision of 258,000 jobs has not only rattled markets, but also led President Trump to fire the head of the Bureau of Labor Statistics – raising fresh concerns about political interference in official data. They explore what this means for the Fed, as a key resignation opens the door for a Trump- aligned appointee and fuels speculation ahead of September rate decision.

Closer to home, where softer inflation and signs of labour market weakness have markets fully pricing in a rate cut at tomorrow’s RBA meeting.

Listen on Apple Podcasts

Watch on YouTube