SB News - February 2026

Capital Gains Tax back in the spotlight

Australia’s capital gains tax discount has moved firmly back into the policy spotlight. Introduced in 1999 as part of the Howard Government’s response to the Ralph Review of Business Taxation, the 50 per cent CGT discount replaced the prior indexation regime. Before 1999, investors were taxed on their real gains, with the asset’s cost base adjusted for inflation. The shift to a flat discount was designed to simplify administration, account for inflation and investment risk, and encourage long-term capital formation. Since then, the 50 per cent discount for individuals and trusts, and the one-third discount for superannuation funds, has become embedded in Australia’s investment framework, shaping decisions across property, equities, private business ownership, and private markets.

Recent reporting highlights growing debate within government about whether the current settings remain appropriate. The issue is closely linked to housing affordability, tax equity, and budget sustainability. A Senate Select Committee, established in November and led by the Greens, is examining the role of tax concessions, including the CGT discount, in driving housing outcomes and wealth inequality, with its report due in March 2026. Senior ministers have not confirmed any change, but nor have they ruled reform out. Treasurer Jim Chalmers has confirmed the government is considering “tax options” to address housing affordability and intergenerational inequality ahead of the May federal budget. Finance Minister Katy Gallagher has said it is “appropriate” to look at adjusting CGT concessions. At the same time, Treasury officials have told parliamentary committees that changes to CGT alone may have only modest effects on housing supply or prices, suggesting any reform would need to be considered alongside broader structural measures.

What form could changes take?

Several reform pathways are being discussed in policy circles:

- A reduction in the discount from 50 per cent to around 33 per cent, which Treasury has reportedly been modelling as a leading option ahead of the May budget, according to the Australian Financial Review. Notably, a source indicated the government’s preferred approach would not apply retrospectively.

- A tiered discount based on holding period, to further reward long-term investment.

- Reintroduction of inflation indexing of the cost base, which would tax real gains rather than nominal gains, an approach reportedly advocated by NSW Treasury among others, as superior to a flat rate reduction.

- Targeted adjustments by asset type – for example, reducing the discount for residential investment properties while retaining a higher rate for shares or new housing construction, to address affordability without undermining supply incentives.

Any significant change would likely involve transitional arrangements, either grandfathering existing holdings or phasing new rules in over time. Sources close to the government suggest grandfathering is likely, though this is not guaranteed and remains actively debated.

What would it mean for investors?

A reduction in the CGT discount would raise the effective tax rate on realised gains for individuals and trusts. Under current settings, an individual on the top marginal rate pays tax on only half their capital gain. If the discount were reduced to 33 per cent, the taxable portion would increase materially and the effective tax payable on a sale would rise noticeably. For property investors in particular, this changes the equation on after-tax returns and may influence decisions about timing of sales or holding periods. It would also interact with negative gearing provisions, which allow investment losses to be offset against other income. The Parliamentary Budget Office estimates the CGT discount will cost the federal budget $247 billion over the next decade, with significantly over half of the benefit accruing to the top decile of income earners. The analysis was commissioned by the Greens-led Senate Select Committee into the Operation of the CGT Discount.

Political debate is already underway. Opposition figures have labelled potential CGT reform a revenue grab that could worsen housing challenges if poorly designed. While many economists argue the concession unfairly benefits wealthier and older investors and contributes to intergenerational inequality. There are also widespread calls for any reform to be balanced with other tax changes, including income tax cuts, to improve overall equity.

A measured approach

At Stanford Brown, our focus is on how potential policy changes intersect with long-term financial objectives, not on reacting to speculation on prospective policy changes. Tax settings inevitably evolve as governments respond to fiscal pressures, demographic trends, and economic priorities. Attempting to time markets or investment decisions around potential reforms can lead to suboptimal outcomes. Instead, we emphasise resilient portfolio structures with the flexibility to evolve alongside your objectives, regardless of the prevailing tax settings.

Understanding that capital gains tax applies only on realisation, and weighing it alongside diversification, risk management and time in the market, remains central to sound investment planning. The current debate around the CGT discount is part of a broader conversation about fairness, housing affordability, and the long-term sustainability of the tax base. If you would like to explore how potential changes may affect your circumstances, we would be pleased to discuss the implications and options with you.

Source; Australian, AFR

By Vincent O’Neill, CEO

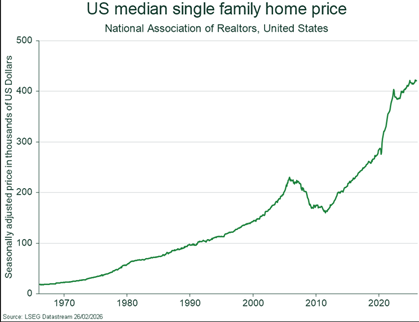

Wall Street vs. Main Street: Battle Over America’s Single-Family Homes

When discussing housing affordability in the United States, few topics currently generate as much debate as the expanding presence of large investment firms in the single-family housing market. So much so that, President Trump has put forward a proposal aimed at limiting how many of these homes institutional buyers can purchase, an idea that has been drawing major attention from economists, investors and prospective homeowners.

For years, institutional investment firms have poured billions into residential real estate, snapping up homes in fast growing regions and transforming them into rental properties. In certain cities, entire neighbourhoods have shifted from owner-occupied homes to corporate-owned rentals. The large presence of institutional buyers has fuelled bidding wars, driven up prices, and ultimately locked first-time buyers out of the market, leaving many with no option but to rent.

The purpose of the proposed policy is to put a cap on the number of single-family properties that large institutional buyers (such as private equity firms and real estate investment trusts) can own. The objective is to curb competition from well capitalised corporations capable of outbidding prospective first-time buyers with all cash offers, buyers who, by contrast, typically rely on financing and are now having to contend with elevated borrowing costs.

Critics, however, caution that the proposal may carry unintended consequences. Institutional landlords play a significant role in providing professionally managed rental housing at scale, while also deploying capital to rehabilitate distressed properties that individual buyers may be unwilling or unable to take on. Limiting their participation, could actually constrain overall housing supply, narrow rental availability, and potentially lead to further price rises. Nonetheless, the political appeal of such a proposal is clear. By targeting institutional buyers, the proposal positions Trump as confronting Wall Street interests in defence of ordinary Americans, where housing costs dominate conversations.

It is important to note that the proposed policy remains in its early stages, and institutional investors expect that any final legislation that is ratified, will differ materially from the framework that has initially been tabled. Institutions have already begun lobbying government officials to advocate for amendments, and early signs suggest that revisions and carve-outs are already in place. These include a limit on additional purchases of single-family homes but would permit the ongoing ownership of them. It also includes exemptions for build-to-rent as well as refurbish-to-rent projects. As a result, investors believe that the current share price weakness being seen in global property managers with substantial exposure to U.S. single-family homes (i.e. American Homes 4 Rent & Invitation Homes) is overblown and in fact could present a great investment opportunity once the regulatory environment becomes clearer.

By Joseph Nakhoul, Investment Research Analyst

From Record Highs to Historic Crash: Precious Metals’ Extraordinary February

Few asset classes have delivered a sharper lesson in momentum risk this year than precious metals. Gold reached an intraday all-time peak of $5,608 per troy ounce on 29 January, nearly double its level a year earlier, before collapsing more than 9% in a single session the following day. It was the steepest one-day fall for the metal since 1983. Silver’s move was more violent still, losing over 31% on 31 January, the worst daily performance since 1980, having briefly traded above $130 before retreating toward $83.

The immediate trigger was President Trump’s nomination of Kevin Warsh to succeed Federal Reserve Chair Jerome Powell. Warsh’s hawkish monetary record was read as a signal of tighter policy ahead, pushing the dollar up around 0.8% and raising the opportunity cost of holding non-yielding bullion. CME Group simultaneously hiked margin requirements on gold from 6% to 8% and silver from 11% to 15%, forcing leveraged speculators to inject capital or close positions at speed. What might have been a correction became a cascade.

The bounce back has been sharp. Gold reclaimed $5,000 by 4 February and was trading around $5,070 by mid-month. Deutsche Bank reiterated its $6,000 year-end target within days, arguing nothing in the pullback had changed the metal’s underlying story. That story rests on several pillars: China’s central bank extended gold purchases for a fifteenth consecutive month in January; softening US data has markets pricing in up to three Fed rate cuts this year; geopolitical risk premiums remain elevated amid US-Iran tensions.

A Reuters poll of 30 strategists placed the median 2026 gold forecast at $4,746, the highest annual consensus in the poll’s history. Goldman Sachs targets $5,400 by year-end while UBS puts its base case at $6,000, with a $7,200 scenario if geopolitical conditions worsen materially. Silver is viewed with considerably more caution. In a 10 February note, J.P. Morgan highlighted the absence of a central bank bid floor comparable to gold’s and noted that with roughly 60% of silver demand tied to industrial use, the metal is far more exposed to any economic slowdown. The bank said it remained reluctant to re-engage until speculative excess had more clearly cleared.

For investors with meaningful commodity allocations, the key question remains whether the case for precious metals, dollar debasement, reserve diversification and a more fractured geopolitical order, justifies the volatility profile both metals now carry. Syz Group’s CIO noted that gold accounts for only around 3% of global AUM across equities, fixed income and alternatives, with a plausible path to 5-10% as institutional reallocation continues.

Source:

CNBC, Gold and Silver Sell-Off: Historic Plunge (2 February 2026)

CNBC, How to Trade the Market Spiral (2 February 2026)

J.P. Morgan Global Research, Silver Prices 2026 (10 February 2026)

Trading Economics, Gold Spot Price Data (February 2026)

Finance Magnates, Gold Price Prediction 2026 (February 2026)

deVere Group, 2026 Gold Outlook (February 2026)

CFI Trade, Gold and Silver Forecast February 2026

By Joey Mouracadeh, Senior Investment Director

Private Credit Faces Its AI Reckoning

February has been an uncomfortable month for private credit. What started as a selloff in public software stocks worked its way through the financial system and onto the balance sheets of business development companies. Blue Owl Capital was at the centre of it, though its story is more complicated than the headlines suggested.

On 2 February, the day after Anthropic’s Claude Cowork launch triggered a wave of software selling, BDC shares fell sharply. Blue Owl Capital Corp ended the session down more than 4%, its lowest since October 2022. Ares, Sixth Street and Trinity Capital all fell. The fear was simple: if AI was going to hollow out enterprise software companies, private credit funds that lent heavily to those businesses were sitting on a problem. Software loans make up around 20% of public BDC portfolios according to Barclays. Blue Owl disclosed on its Q4 earnings call that more than 70% of its loans go to software companies. By 6 February, Bloomberg reported bond dealers were demanding higher compensation to trade BDC corporate debt, a sign unease was spreading from equity markets into the funding stack.

UBS warned that in an aggressive AI disruption scenario, private credit default rates could climb to 13%, well above stress estimates of 8% for leveraged loans and 4% for high yield. PitchBook showed software accounting for 17% of BDC investments by deal count. Payment-in-kind loans, concentrated in software, drew additional concern: PIK structures let borrowers defer cash interest and turn risky quickly if revenues weaken.

The Blue Owl OBDC II announcement on 18 February reignited things. The fund, raised in 2017 with a planned end-of-life liquidity event, sold $1.4 billion of loans after a merger with OBDC was abandoned last year. OBDC II investors will receive roughly 30% of NAV in cash by 31 March, far larger and faster than the 5% maximum through standard quarterly tender offers. The loans were sold at 99.7% of par to CalPERS, Ontario Municipal Employees Retirement System, BC Investment Management and insurer Kuvare. Four institutions with every reason to scrutinise the assets chose to buy at close to face value. KBRA, which rates OBDC II BBB+, said the deal demonstrated the manager’s ability to mark its book accurately.

Current credit metrics support a measured reading. OBDC’s non-accruals fell to 2.3% in Q4 from 2.7% in Q3. Ares noted software loans represent roughly 6% of its total assets. Goldman Sachs does not see systemic risk from non-traded BDC redemptions, pointing to around $400 billion in unlevered institutional dry powder available, and noting non-traded BDCs run at 0.7x leverage versus 0.9x for publicly traded peers.

The tension is not between a functioning asset class and a failing one. It is between a market absorbing a legitimate question about software credit quality and a body of reported facts that do not yet support the worst-case reading. As one private credit lender told 9fin, the AI selloff makes you want to re-examine the most exposed names, even if the numbers do not yet demand it.

Source:

CNBC, Private Credit Stocks Plummet on Concern About Exposure to Software (3 February 2026)

Bloomberg, Private Credit-Linked Shares Drop on Software Exposure Concerns (2 February 2026)

Bloomberg, Private Credit Stocks Keep Falling as Software Wipeout Spreads (6 February 2026)

Bloomberg, Bond Dealers Push Up Private Credit Fund Trading Costs Amid Software Slide (10 February 2026)

CNBC, Private Credit Worries Resurface in $3 Trillion Market as AI Pressures Software Firms (9 February 2026)

CNBC, Illiquid Loans, Investor Demands: Blue Owl’s Software Lending Triggers Another Quake (20 February 2026)

9fin, Private Credit Defends Software Exposure Amid Sector Selloff (February 2026)

Cliffwater LLC / Larry Swedroe, Blue Owl, OBDC II and the Private Credit Panic That Wasn’t (20 February 2026)

KBRA, KBRA Comments on Blue Owl Capital Corporation II’s Asset Sales (February 2026)

CNBC, Private Credit’s Golden Era Over? Timeline of the Industry’s Cracks (24 February 2026)

By Joey Mouracadeh, Senior Investment Director

AI Doom

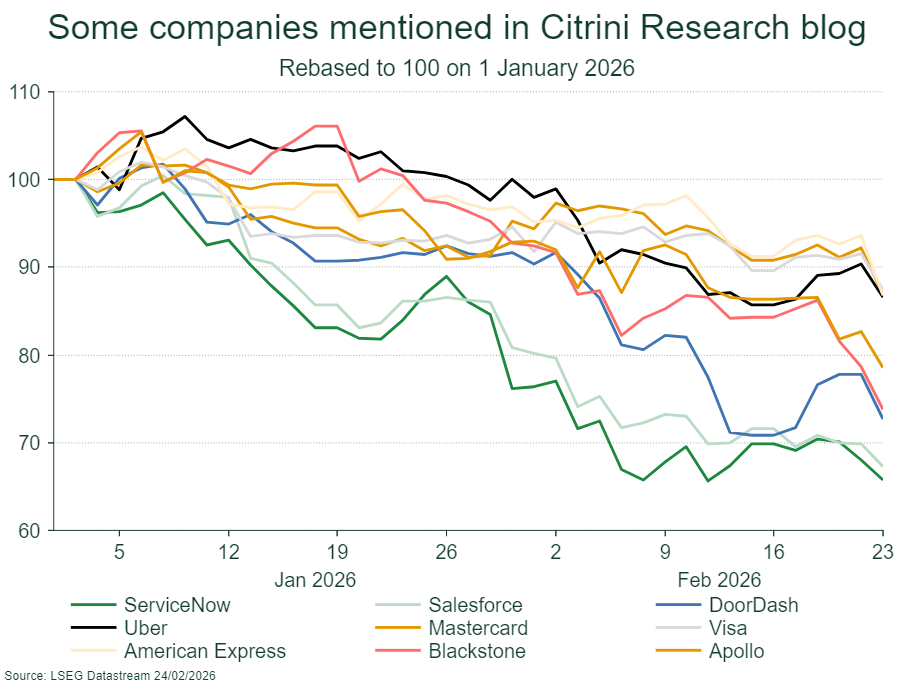

A viral blog post written last weekend, as a thought experiment about an Artificial Intelligence-driven future, sent shockwaves through financial markets, offering a doomsday vision where the very success of AI triggers a global economic collapse. The report, titled “The 2028 Global Intelligence Crisis,” was co-authored by Citrini Research and tech entrepreneur Alap Shah. Written as a fictional macroeconomic report from June 2028, it describes a world where AI and machine intelligence has become so cheap and abundant that it has rendered human intelligence and white-collar labour – and the consumer economy it supports – obsolete.

The central thesis of the crisis is the “Human Intelligence Displacement Spiral.” The 2028 report states that by late 2025, AI had reached a capability that allowed companies to replace millions of white-collar professionals. While corporations initially saw record profit margins and share price gains from AI adoption, the subsequent worker layoffs eventually backfired on companies. White-collar workers, who in the United States drive roughly 75% of discretionary consumer spending, lost their earnings power, triggering a massive contraction in economic demand.

Economists in 2028 dubbed the resulting productivity boom “Ghost GDP”. While machines boost productivity and GDP expands to record levels, the additional national income fails to circulate in the economy because, as the report puts it, “machines spend zero dollars on discretionary goods”. The speed at which money changes hands in the economy has slowed, and human consumption, which had accounted for 70% of US GDP, has contracted. In this possible future, by mid-2028 the US unemployment rate has surged above 10%, and the stock market has declined around 40% from its 2026 peak.

The report outlines how AI disruption hollowed out industries once thought immune. In enterprise software, companies face a “race to the bottom” as AI coding tools turn projects, that once took months to build using thousands of engineers, into tasks completed in hours. This has allowed competitors to easily launch similar products, erasing brand differentiation. Clients of these software firms have also used AI to cut headcount and then automatically cancel their per-seat software licenses, destroying the software industry’s revenues. To protect profit margins, companies cut costs further by increasing their AI use, creating a reflexive “doom loop”.

Similarly, the “death of friction” hits banks and payment giants like Visa and Mastercard. AI agents, optimising for low cost, speed and efficiency, have begun making payments through frictionless stablecoins, bypassing the 2-3% interchange fees that once underpinned banking and the global payments system. In the real estate sector, commission structures have collapsed due to “agent-on-agent violence” where AI agents equipped with decades of data have compressed median buy-side commissions from 3% to under 1%. As the report notes, “Humans don’t really have the time to price-match across five platforms… Machines do,” effectively ending business models built on human inertia.

The contagion has now reached credit markets. In late 2027, the default of a US$5 billion loan to software firm Zendesk sent ripples through the private credit market, with losses flowing to insurance companies and holders of annuities. The US$13 trillion US residential mortgage market is also under stress. While the blue-collar and gig sectors were initially safe, they have been hit by a flood of displaced white-collar professionals looking for work, causing wages to plunge across the entire economy. Globally, the threat is existential for service nations like India, where the export of software development and call centre labour is being substituted by near-zero cost AI agents.

While the report is explicitly framed as a “thought experiment” and exploration of one possible scenario rather than a forecast, it triggered a real-world market selloff in the shares of many tech firms, asset managers, and payment companies. Investors, already uneasy about high valuations and the impact of AI have adopted a “shoot first, ask questions later” herd mentality. Shares in companies mentioned in the report like Visa, Mastercard, DoorDash, Blackston, Apollo and ServiceNow were sold off. The market response suggests that even if the 2028 scenario never eventuates, fear of such a scenario is enough to trigger a repricing of companies in “intelligence” related industries.

Critics of the Citrini report argue that the concept of “Ghost GDP” doesn’t make a lot of sense – if the economy is growing because of an AI-driven productivity surge, then it cannot also be in recession – the income needs to be going somewhere and investment activity, exports and/or government spending need to be growing strongly to make up for the consumer spending shortfall. Other critics argue that as with prior technological revolutions new industries inevitably emerge to absorb displaced workers, even if we don’t know what those industries look like today. One thing is clear, which is that the blog post landed at a time when investors are nervous about where the AI revolution takes us and plays into ancient fears about robots replacing human workers.

By Nick Ryder, Chief Investment Officer

Peak Trump

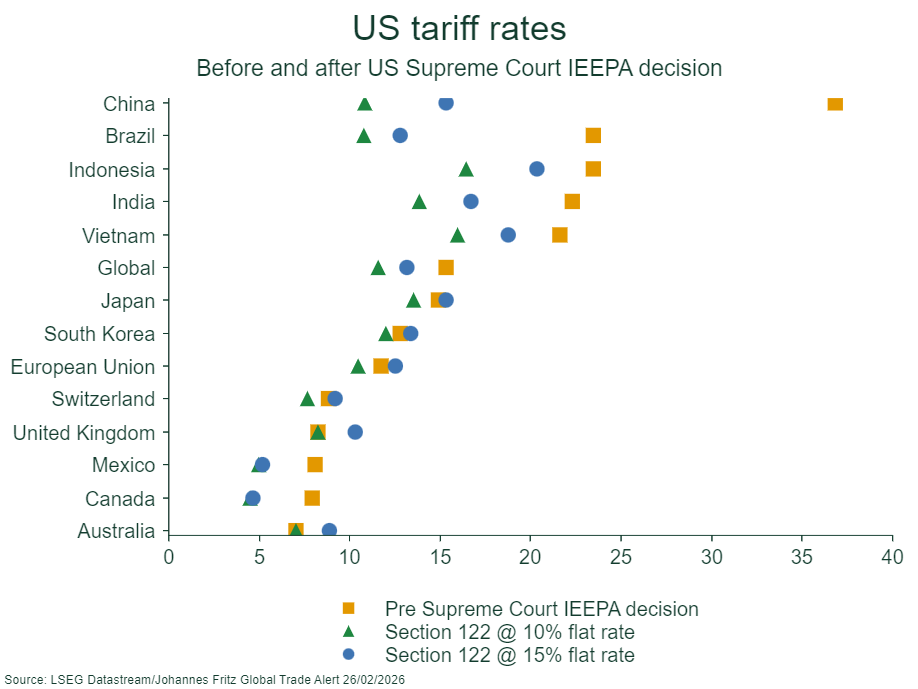

Global trade has once again been thrown into a state of chaos after a landmark 6-3 ruling from the US Supreme Court invalidated the US President’s use of the International Emergency Economic Powers Act (IEEPA) to impose last year’s broad-based reciprocal and fentanyl-related tariffs. Writing for the majority, Supreme Court Justice Gorsuch reinforced the constitutional separation of powers, asserting that the authority to tax – tariffs being a form of tax – rests solely with Congress, not the executive branch. Analysts suggest this ruling marks the end of “Peak Trump,” signalling that the president is now increasingly being constrained by the courts and a more assertive Congress as the US heads towards November’s mid-term elections.

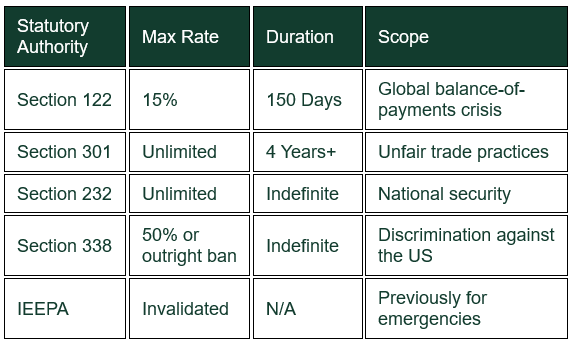

President Trump immediately responded to the court ruling by invoking Section 122 of the Trade Act of 1974, a dormant 1970s provision that was designed in a period of fixed exchange rates to cover balance-of-payments emergencies. This is likely also on shaky legal ground given the US is not currently experiencing such an emergency. US Customs and Border Protection began collecting the new levy at a 10% rate on 24 February 2026, however, White House officials clarified that the 10% rate is temporary while the administration works to hike the duty to the statutory maximum of 15% in coming days. These measures are legally capped at 150 days, meaning they will expire on 24 July 2026, unless Congress extends the tariffs, which is regarded as highly unlikely.

The shift from the flexible IEEPA framework to a blunt Section 122 surcharge has created another spike in global trade uncertainty after the chaos from the “Liberation Day” tariff announcements in April 2025. Paradoxically, strategic rivals like China have emerged as relative winners as their effective rate will decline with high IEEPA tariffs replaced by the uniform 10% or 15% cap, restoring some price competitiveness for Chinese consumer goods. Conversely, allies like Australia and the UK are the main losers given both countries negotiated 10% tariff rates in 2025, which could now be effectively nullified by the 15% global floor.

The court decision and introduction of the Section 122 tariffs have also jeopardised all the bilateral trade agreements put in place last year. European policymakers urgently froze ratification of the “Turnberry Agreement” trade deal they signed with the US in July 2025 that had a 15% tariff rate ceiling on European imports in exchange for US$600 billion in manufacturing investments. Japan faces similar uncertainty regarding its US$550 billion investment package, as Japan’s Prime Minister seeks assurances that Japanese exports will receive treatment as favourable as their existing framework agreement signed last year.

While the Section 122 tariffs are likely to be temporary, the US administration is already preparing more durable tariff replacements. US Trade Representative Jamieson Greer indicated that the White House will soon move forward with new investigations under Section 301 and Section 232. These replacements, which were used by both the Trump and Biden administrations previously, will target forced labour, industrial subsidies, and national security threats, allowing the administration to recreate the previous tariff landscape through more legally robust, but more cumbersome, provisions.

Additionally, the administration is eyeing Section 338 of the Tariff Act of 1930, a Great Depression-era tool not invoked since 1935 that allows for 50% tariffs or total import bans on countries deemed to be discriminating against US commerce. While more legally dubious, given it being untested in modern law and lacking procedural safeguards, officials view it as a potential weapon for “maximum aggression”.

The most immediate crisis involves the estimated US$175 billion in IEEPA tariffs already collected by the US Treasury. The Trump administration is reportedly preparing to resist a swift repayment process and over 1,800 companies, including major importers, have already launched legal action against the US government to recover tariff refunds. The Court on International Trade is expected to determine if refunds will be automatic or require a clunky application process for importers. If the full US$175 billion is returned, analysts warn the US government budget deficit could widen by approximately 10%, potentially reaching US$1.9 trillion.

The court decision has created a strategic limbo for multinational companies. Once again businesses are struggling to determine whether to absorb the 10-15% Section 122 surcharge as a temporary cost or to overhaul supply chains in anticipation of the more permanent Section 301 and 232 replacements. While domestic US manufacturing output is projected to expand in the long run due to reshoring, the Federal Reserve Bank of New York has found that 90% of current tariff costs are being borne by American firms and consumers rather than foreign exporters.

Ultimately, the Supreme Court ruling reshapes the office of the presidency. By narrowing the definition of “emergencies”, the Supreme Court has limited the ability of future presidents to effectuate spending and tax policy without congressional intent. Though Trump aims to replicate his ~13% average tariff rate through other means, he now faces a world where his leverage in negotiations has significantly diminished. His trade policy likely remains under constant threat of further litigation and his main foreign policy tool, threatening individual countries with higher tariffs – as he did recently with eight NATO countries over Greenland – is greatly diminished.

By Nick Ryder, Chief Investment Officer

Latest Podcast

SCOTUS Rules and Software Cools

In this episode of SB Talks, CEO Vincent O’Neill and CIO Nick Ryder unpack a landmark US Supreme Court (‘SCOTUS’) ruling that strikes down key Trump-era tariffs, causing trade uncertainty once again. They explore what softer US Q4 GDP numbers really say about the economy, cutting through shutdown noise to assess the health of the consumer, inflation, and interest rate expectations.

The conversation then turns to AI’s accelerating disruption – separating winners from losers across software, equity markets, and private credit. With uncertainty rising but fundamentals holding, the episode offers a grounded, cautiously optimistic take on how investors can navigate a rapidly shifting landscape.