SB News - January 2026

Fed leadership call next week puts bond market and independence in the spotlight

President Donald Trump has signalled that he will announce his nominee for the next Chair of the United States Federal Reserve next week as Jerome Powell’s term approaches its conclusion in May 2026. Markets had already expected an update, and recent commentary suggests the shortlist now revolves around Rick Rieder, Kevin Warsh, Christopher Waller, and Kevin Hassett. Reports also suggest that Waller dissented at the most recent Federal Open Market Committee meeting, which held interest rates steady at 3.5 to 3.75% after three cuts in 2025.

Prediction markets have moved quickly in recent days. Rick Rieder has surged in odds after President Trump described him as very impressive and senior officials signalled openness to selecting an experienced market practitioner. Less than a week ago, Kevin Warsh was considered the strongest possibility, and both Waller and Hassett remain in the mix despite shifting expectations.

Light background on the four leading contenders

Rick Rieder is BlackRock’s Chief Investment Officer for Global Fixed Income and a Senior Managing Director responsible for managing trillions in fixed income assets. He has previously served on the Federal Reserve’s Investment Advisory Committee on Financial Markets and built his career through senior roles at Lehman Brothers and R3 Capital Partners. His deep markets background makes him a nontraditional contender who would bring a practitioner’s perspective to monetary policy.

Kevin Warsh served as a Federal Reserve Governor from 2006 to 2011 and was the central bank’s liaison to Wall Street during the global financial crisis. Prior to his government service, he worked in mergers and acquisitions at Morgan Stanley and later served as an economic adviser in the White House.

Christopher Waller is an economist currently serving as a Federal Reserve Governor. Before joining the Board, he spent ten years as Executive Vice President and Director of Research at the Federal Reserve Bank of St. Louis and previously held academic positions at Notre Dame, Kentucky and Indiana University.

Kevin Hassett, Director of the National Economic Council, is a long-time economic adviser to President Trump with a background spanning academia, government and senior policy roles. He previously chaired the Council of Economic Advisers and has been associated with pro growth policies that place emphasis on lower interest rates and stronger economic momentum.

Fed independence remains the central market concern

While the choice of Chair matters enormously, markets are more preoccupied with the question of Federal Reserve independence. Recent developments, including a Department of Justice investigation into Powell’s testimony concerning a renovation project and an effort to remove Governor Lisa Cook, have raised concern about political encroachment on central bank decision making.

If confidence in the Federal Reserve’s independence were to weaken, investors would likely demand higher compensation for risk. This could push longer term interest rates higher and add upward pressure to bond yields more broadly. Structural factors are also at play, including the volume of government debt being issued, so uncertainty around leadership simply adds another source of market volatility.

What to watch in the bond market

In the days ahead, markets will be watching closely for any signals from the White House and from potential nominees. If investors begin to expect fewer interest rate cuts, borrowing costs tend to stay higher in the near term, while uncertainty around leadership can lead to more swings in longer term markets.

A nominee seen as favouring faster rate cuts could give markets a short term boost. However, if that appointment raises concerns about the Fed’s independence, it could place pressure on the currency, push longer term interest rates higher and gradually undermine market confidence. By contrast, a nominee with strong policy credibility may mean a slower pace of rate cuts, but could provide reassurance and stability at a time when markets value consistency. As always, we will share our views on the implications once the nominee is announced.

By Vincent O’Neill, CEO

RBA Hike or Hold?

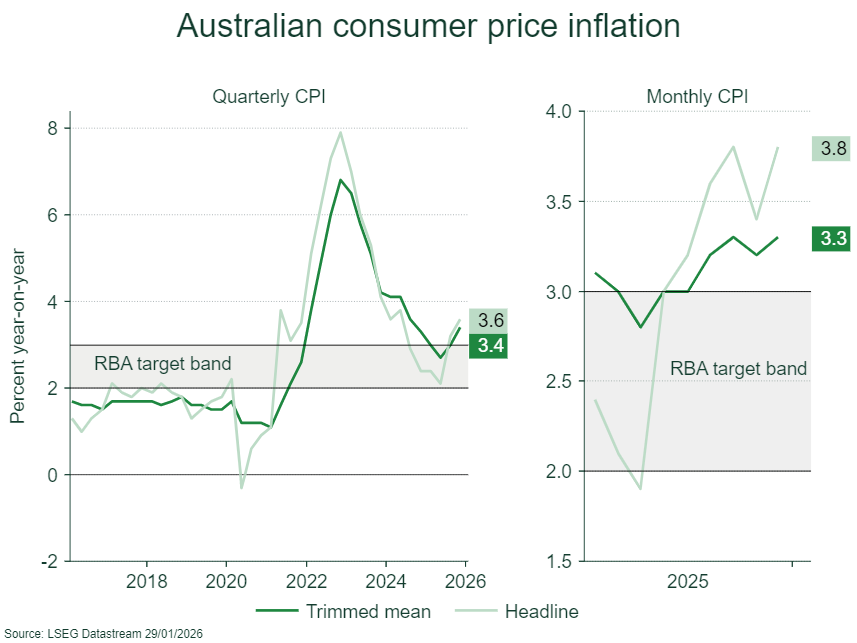

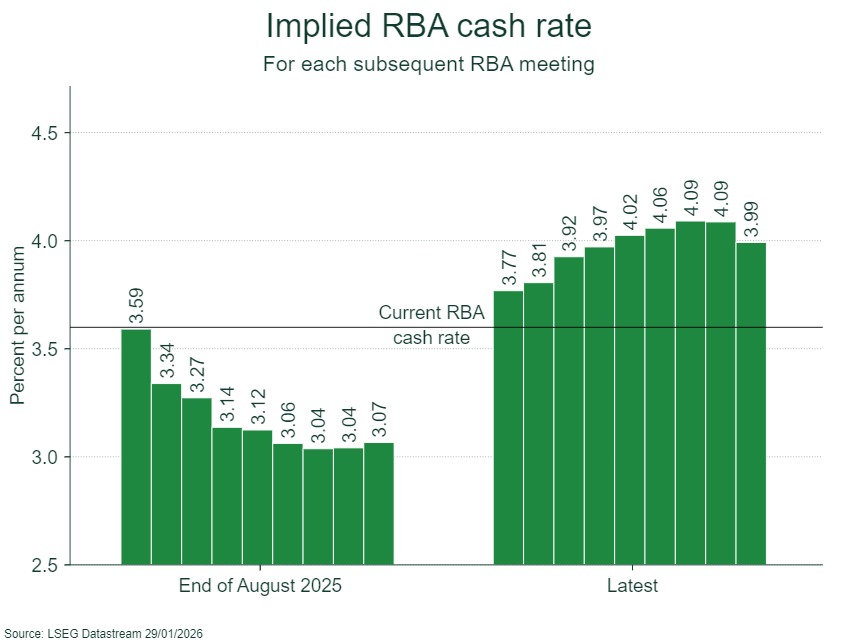

The Australian economic landscape has shifted dramatically over the past few months as the battle against inflation enters a more challenging phase for the Reserve Bank of Australia (RBA) in 2026. Recent data has dashed hopes of further rate cuts, with markets and major lenders now expecting an interest rate hike next week.

This week the Australian Bureau of Statistics confirmed that monthly headline inflation had climbed to 3.8% in the year to December 2025, up from 3.4% in November. This result exceeded market forecasts of 3.6% and remains well above the RBA’s 2% to 3% target range. Crucially, the quarterly trimmed mean inflation, the RBA’s preferred measure of underlying price growth, printed at 0.9% for the December quarter, 15 basis points higher than the RBA’s own forecast made in November.

Housing costs remain the primary driver of persistent inflation pressures, rising 5.5% annually. Within this category, electricity prices jumped 21.5% as state government rebates in Queensland and Western Australia ended. While Federal Treasurer Jim Chalmers has stated these figures are the “very temporary” results of expiring subsidies, RBA Governor Michele Bullock has stated that the Board looked through these effects when the rebates were introduced and will do so again as they roll off. When excluding the impact of rebates, electricity prices still rose a steady 4.6%. Furthermore, services inflation reached a two-year high of 4.1%, driven by a 9.6% jump in domestic travel and accommodation during the summer season.

The RBA’s December meeting marked a definitive hawkish pivot. Governor Bullock revealed that the Board did not consider a rate cut at all during its final deliberations of 2025. Instead, the discussion focused on the circumstances that might necessitate a rate rise in 2026, with the Board becoming increasingly alert to signs of a more broad-based pick-up in inflation. Governor Bullock previously warned that if inflation pressures look persistent and the economy remains out of balance, the Board will not hesitate to take action.

This concern is compounded by recent data that shows the labour market remains tight. The unemployment rate eased from 4.3% to a seven-month low of 4.1% in December, with the economy adding 65,000 jobs, a figure well above economists’ expectations. Deputy RBA Governor Andrew Hauser noted that Australia appears to be “banging up against the constraints of the supply side,” with high capacity utilisation leaving little scope for economic growth without fueling price increases.

After this week’s inflation result, all of Australia’s “Big Four” banks are now forecasting a 25-basis point interest rate hike in February after Westpac and ANZ joined CBA and NAB in predicting a move up to 3.85%. Money markets have a 70% chance of a rate hike next week. However, the consensus view of a February rate hike is being challenged by high-profile holdouts at Goldman Sachs and Deutsche Bank who believe the RBA will remain patient and keep rates on hold.

Goldman Sachs is holding fast to the view that the cash rate will stay at 3.60% throughout 2026, despite the inflation surprise, arguing that the 0.9% quarterly increase in trimmed mean inflation, while higher than the RBA’s previous forecast, does not represent a large enough upside surprise to warrant a sudden shift from an easing bias to an actual rate hike in just three months. Goldman also suggests that the recent appreciation of the Australian Dollar has effectively tightened financial conditions, doing some of the heavy lifting for the central bank. They also argue the current inflation in administered services, food, and fuel is not necessarily a signal of broader capacity constraints.

This cautious outlook aligns with Deutsche Bank’s assessment, which focuses on the cooling momentum seen from the new monthly inflation data series. Deutsche Bank highlights that the monthly trimmed mean actually decelerated for three consecutive months, falling to 0.23% in December. This supports the view that earlier price spikes were driven by temporary factors that are now beginning to unwind. They contend that while the quarterly data appeared “just a tiny bit higher” than RBA expectations, the “dovish” direction of the monthly trend should be weighed equally by policymakers.

The RBA’s reaction function is now the wild card. Governor Bullock has previously signaled that the Board would remain data-dependent. Whether the current combination of hot inflation and a tight labor market means that the RBA hikes in February as a single “insurance” move, or waits a little longer to get more data on the trend in underlying inflation remains an open debate. We’ll find out next week.

By Nick Ryder, Chief Investment Officer

Davos Realpolitik

The 56th Annual Meeting of the World Economic Forum concluded in the Swiss ski resort of Davos last week, serving as a critical international platform where leaders from government, business, and civil society gather to address the world’s most pressing challenges. With a record-breaking attendance of over 3,000 people, including more than 60 heads of state and 1,000 CEOs, this year’s meeting operated under the theme “A Spirit of Dialogue”. Despite the official focus on conversation, the atmosphere was overshadowed by geostrategic uncertainty and the looming reality of what many participants described as a transition from a rules-based system to a power-driven “law of the jungle”.

Central to this year’s event was US President Donald Trump, who used the stage to talk up his first year’s achievements, highlight a booming American economy. Trump’s presence, however, underscored a deepening rift with traditional allies, notably through his controversial ambition to acquire Greenland, which he framed as a core national security interest for the United States. While Trump eventually signaled a shift toward negotiation rather than using military force regarding the island, the incident badly rattled the transatlantic relationship and prompted European leaders like French President, Emmanuel Macron, and European Commission President, Ursula von der Leyen, to call for greater European independence and strategic autonomy.

In a significant counterpoint to Trump’s unilateralism, Canadian Prime Minister, Mark Carney, delivered a speech that was widely regarded as a moral reference point for middle powers and smaller nations. Carney declared that the rules-based international order had experienced a “rupture, not a transition,” and we are at the beginning of a “brutal reality” where great power geopolitics are no longer subject to constraints. He warned that great powers have begun to exploit economic integration using tariffs as leverage, financial infrastructure for coercion and supply chains as vulnerabilities to be exploited.

*Image source generated by copilot

By Nick Ryder, Chief Investment Officer

South Korea Overtakes Germany in Market Value as Tech Boom Reshapes Global Equity Rankings

South Korea has recently surpassed Europe’s largest economy, Germany, in total stock market value, highlighting the growing influence of technology driven markets in the global economy. The South Korean equity market has reached a total valuation of approximately US$3.25 trillion, more than doubling since the start of 2025. This now places the country ahead of Germany, whose market valuation stands at US$3.22 trillion, making South Korea the world’s 10th largest stock market by size, just behind Taiwan.

The rapid growth of Korean equities has been fuelled by shareholder friendly reforms and the country’s central role in the global supply chain for artificial intelligence and advanced technologies. The Kospi Index has climbed roughly 20% in 2026 alone, sharply outperforming Germany’s DAX Index, which has gained just 1.2% amid geopolitical uncertainty.

South Korea has strategically positioned itself at the centre of three powerful long-term themes, artificial intelligence, electrification, and defence allowing it to benefit from AI infrastructure investment, rising semiconductor demand, and increased global defence spending. Contrastingly to Germany, where corporate earnings are facing structural pressures from a slowdown in its automotive and chemicals industries.

Support from President Lee Jae Myung, who has championed stock market development and corporate governance reforms, has further boosted investor confidence in South Korea. This, in addition to supply shortages and rising prices of memory chips has driven strong gains in heavyweights such as Samsung Electronics and SK Hynix, which has helped push the Kospi Index above the 5,000 level for the first time in its history. The technology sector now accounts for around 40% of the Kospi Index, in stark contrast to Germany’s DAX Index, which leans more heavily toward the industrials sector. Although German stocks saw early gains in 2025 on expectations of large-scale government stimulus, uncertainty around the timing and allocation of potential spending (estimated at up to €1 trillion), has seen investor sentiment wane, whereas South Korea’s dominance in semiconductors and advanced manufacturing has now given it a decisive market edge.

Given how swiftly market dynamics can change, it is critical to partner with investment managers who have the ability to allocate capital globally and within niche markets. This enables managers to dynamically allocate across countries as new opportunities emerge, positioning portfolios to benefit from structural change and dislocation. Furthermore, managers with on-the-ground presence in various capital cities across the world, often develop insights into changing policy, regulatory shifts, and economic trends ahead of other broader market participants. This edge can allow them to position portfolios proactively, capturing investment opportunities early and enhancing the potential for outsized investor returns.

By Joseph Nakhoul, Investment Research Analyst