SB News - May 2026

Federal Budget 2026–27: Where to from here?

The May Federal Budget proposes some of the most significant changes to Australia’s tax system in decades. While many of these measures are not scheduled to take effect for some time, the potential implications for how families, investors and business owners structure their affairs are substantial. For many Australians, this is not a Budget that can simply be revisited closer to implementation.

A proposed new capital gains regime

One of the most significant proposals is the removal of the 50% capital gains tax discount from 1 July 2027 for individuals and trusts. There is no change to the existing 33.33% capital gains discount applying to superannuation funds.

In its place would be a system of cost base indexation for assets held for more than 12 months, together with a 30% minimum tax on realised net capital gains. Notably, investors in new residential properties will retain the option to choose between the new regime and the existing 50% CGT discount, which may be relevant to future investment decisions.

The Budget also proposes applying the new CGT regime to pre-CGT assets, that is, assets acquired before 20 September 1985.

Under transitional arrangements, there will be no changes in arrangements for assets purchased and sold prior to 1 July 2027. For assets owned prior to 1 July 2027, gains that accrued before 1 July 2027 will remain entitled to the 50% discount and taxed at the taxpayers marginal tax rate, but gains arising from that date onward will be subject to the new rules.

For many investors, the CGT discount has been a fundamental component of long-term investment planning. Its proposed removal may influence decisions around asset ownership, portfolio construction, succession planning and the timing of future transactions. There will also be important implications for affected families and business owners.

Changes to negative gearing

The Government has also proposed significant changes to negative gearing concessions for residential property, with future access largely restricted to newly constructed properties. It is worth noting that negative gearing on non-residential assets, such as shares and commercial property, is not affected by these changes. From 1 July 2027, losses from established residential properties will only be deductible against rental income or the capital gains from residential properties (not from other forms of taxable income such as salary and wages).

While existing arrangements are expected to be grandfathered for properties owned (or with contracts exchanged) before Budget night, the proposed rules may alter the economics of future property investment and influence how investors compare residential property with alternative income-producing assets.

Discretionary trusts under review

For private business owners and family groups, perhaps the most consequential proposal relates to discretionary trusts.

From 1 July 2028, a 30% minimum tax is proposed to apply to discretionary trust income, collected at the trustee level. Non-corporate beneficiaries will receive non-refundable credits for their share of the tax paid by the trustee, which can offset their own tax liabilities. However, no such credits will be available where distributions are made to corporate beneficiaries, a deliberate integrity measure aimed at discouraging the use of so-called “bucket companies”. Depending on individual circumstances, this could materially increase the overall tax burden for some trust structures.

For businesses considering restructuring, it is worth noting that rollover relief will be available for three years from 1 July 2027 for eligible small businesses wishing to restructure out of discretionary trusts into other entity types, such as a company or fixed trust.

Given the widespread use of discretionary trusts across Australia, these changes have the potential to influence how family groups, investment structures and private businesses are organised in the years ahead.

Some positive measures

The Budget does contain several initiatives aimed at encouraging innovation and investment.

The R&D Tax Incentive has been amended to increase the minimum expenditure threshold to $50,000, meaning R&D expenditure below this amount must be undertaken through a Research Service Provider or Cooperative Research Centre. Venture capital settings have also been expanded, providing additional support for early-stage investment activity.

While these measures will be welcomed by affected businesses, they are likely to be of more limited relevance for many families and investors than the broader tax reforms proposed elsewhere in the Budget.

Where to from here?

Although the implementation dates remain some distance away, the complexity of many of these proposed changes means that early planning is likely to be valuable.

The next 18 to 24 months may provide an important window to review structures, model potential outcomes, and consider whether any changes are appropriate. Importantly, there is no need for immediate action in most cases, but there is considerable value in understanding how the proposals could affect your specific circumstances.

As always, we will continue to monitor developments closely and will keep you informed as further detail emerges.

If you would like to discuss what these proposals may mean for you, please do not hesitate to contact us.

By Vincent O’Neill, Chief Investment Officer

Quantum Threat

A Google whitepaper released last month has marked a watershed moment for global financial security, signalling a definitive shift in the perception and timing of security threats from quantum computers. Virtually all modern digital security – from online banking and secure messaging to the private keys that safeguard cryptocurrencies – relies on mathematical problems that are incredibly difficult for standard computers to solve. However, a sufficiently powerful quantum computer could solve these problems in a matter of minutes, rendering current encryption obsolete.

Once dismissed as a “distant, academic concern,” the emergence of cryptographically relevant quantum computers (CRQCs) is now framed as a credible, near-term risk by the Google paper. This acceleration is partly driven by Google’s “Willow” quantum chip, which demonstrated the ability to solve in five minutes what would take classical supercomputers approximately ten septillion (i.e. 10 followed by 24 zeros) years. The improvement in quantum computing is also being assisted by AI assisted error correction software that use machine learning to make quantum computers far more accurate.

While standard computers use binary “bits” which acts like a light switch and must be definitively in one state: either a 0 or 1, a quantum computer uses “qubits” which acts like a dimmer switch where it can be 0, 1, or any proportion of both at the same time. This means quantum computers can handle calculations involving much larger volumes of data, theoretically enabling them to unscramble the multiplications of large prime numbers that underpin existing cryptography.

Modern cryptography relies on an asymmetric rule: some mathematical operations – such as multiplication of large prime numbers to generate what is referred to as a public key – are incredibly easy to do in one direction, but brutally difficult for a standard computer to perform in reverse, using step by step guessing, unless you have a specific piece of secret information – referred to as a private key or one of the prime numbers used in the original multiplication.

The Google paper modelled a scenario in which a quantum computer cracks a Bitcoin private key in approximately nine minutes after a transaction exposes the corresponding public key. That window gives an attacker a 41% probability of completing the theft before Bitcoin’s 10-minute block confirmation closes. The paper estimates roughly 6.9 million Bitcoin, around one-third of total supply worth US$500 billion, sits in wallets where the public key has already been exposed. While the cryptographic algorithm used to mine and create new Bitcoins remains relatively resilient to quantum attacks, the asymmetric signatures securing wallets and ownership are defenceless.

Post-quantum cryptography (PQC) does not rely on quantum physics to secure data, instead, PQC is just smarter maths run on standard computers. Instead of factoring large numbers, PQC algorithms use mathematical structures that quantum computers are not naturally equipped to break. The most popular approach is lattice-based cryptography that hides data inside grids or lattices containing billions of points and asks for the computers to find the shortest vector between the data points that neither standard not quantum computers can solve efficiently.

However, the primary hurdle to quantum resistance is not mathematics, but a “governance gap” in coordination. Bitcoin faces a crisis of ossification with no agreement yet on proposals such as hiding public keys and effectively freezing coins that don’t migrate into new quantum secure wallets. Without a central authority, Bitcoin’s “leaderless” nature turns such a transition into a constitutional risk. The Ethereum Foundation is actively pursuing a post quantum roadmap by 2029 as are companies such as RippleX and stablecoin issuer Circle. However, all these networks face the “defensive downgrade paradox”: migrating to PQC results in a 95% to 99% reduction in transaction throughput given PQC involves much larger signature sizes which reduce the number of transactions contained in each block added to the blockchain. This will inevitably cause fees to spike and transaction speeds to slow, testing the community’s commitment to security.

Meanwhile, some crypto organisations remain sceptical of the quantum threat saying it remains theoretical, that such a quantum computer doesn’t exist yet and could be decades away. Others suggest the threat may be getting closer aided by artificial intelligence improvements and pointed to Nvidia which recently launched new AI models to “accelerate the path” to quantum computers. As with Y2K, major tech infrastructure companies, cybersecurity tools (like OpenSSL used to encrypt internet traffic and email), and financial networks are already integrating PQC algorithms into their systems to ensure a smooth transition before “Q-Day”, the day a quantum computer capable of breaking current encryption is officially turned on.

By Nick Ryder, Chief Investment Officer

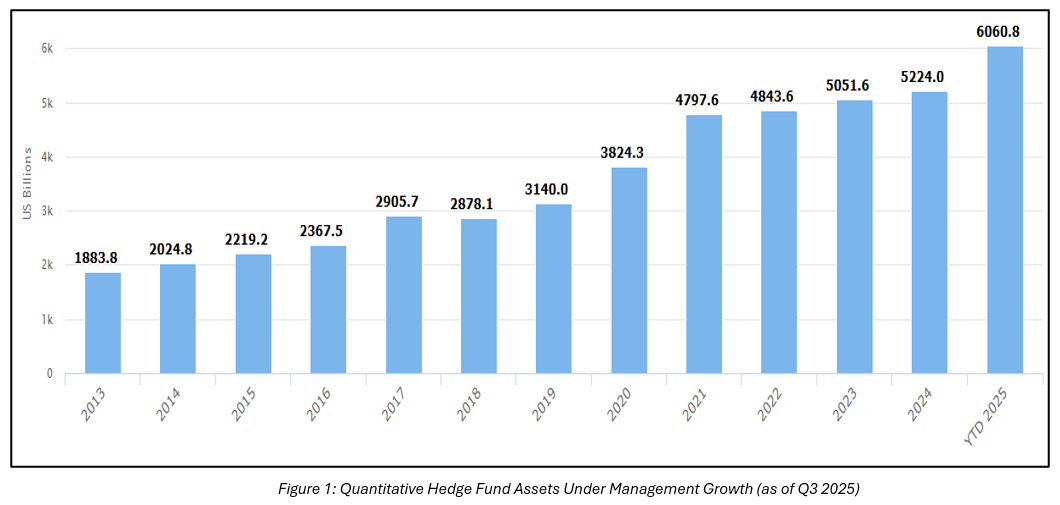

The Rise of the Machines – Why Quantitative Hedge Funds are Thriving in Turbulent Markets

In a market environment defined by shifting interest rate expectations, geopolitical uncertainty and sharp swings in investor sentiment, some of the world’s largest hedge funds have quietly continued to deliver. Quantitative multi-strategy hedge funds; sophisticated investment firms that combine data-driven models and diversified trading strategies have emerged as some of the strongest performers. Unlike traditional investment managers that may rely heavily on stock selection or macroeconomic forecasts, quantitative multi-strategy firms operate across hundreds of markets, with positions spanning equities, fixed income, commodities, currencies and derivatives. Their edge lies in extracting signals from enormous volumes of market data and rapidly adjusting exposures as market conditions evolve.

Over the last few years, this approach has largely benefited from an unusually supportive backdrop. Elevated interest rates, persistent inflation concerns and diverging global economic outcomes have created greater market dispersion, an environment where securities increasingly move independently from one another. For quantitative traders, these conditions can generate a richer opportunity set. Industry heavyweights including Citadel, Millennium, and Point72 have continued attracting significant investor capital, reinforcing demand for strategies capable of navigating both rising and falling markets. While performance has varied across managers, many large multi-strategy platforms have demonstrated resilience through these periods that have challenged more traditional portfolio approaches.

The hedge fund industry however has become an arms race built around technology, talent and data. Firms are investing heavily in artificial intelligence capabilities, alternative datasets, cloud computing infrastructure and increasingly specialised research teams in pursuit of incremental trading advantages against their peers. This rapid evolution has raised the barriers to entry within the industry. Running a global multi-strategy platform requires substantial operational scale, deep risk controls and the ability to recruit and retain elite talent. At the same time, the sector is prone to certain risks. As capital flows into similar strategies, concerns around crowding and capacity have grown. When many firms pursue overlapping trades or signals, performance can become vulnerable. Managing leverage, liquidity and portfolio concentration therefore remains critical.

Recent market conditions have reinforced the appeal of diversified alternatives strategies. For Australian investors, this trend is becoming increasingly relevant. Historically, access to leading global quantitative hedge funds and alternative investment strategies has largely been confined to institutional investors and ultra-high-net-worth individuals. However, the emergence of alternative investment vehicles, feeder funds and more accessible investment structures is gradually democratising access to these sophisticated strategies.

Recognising the growing importance of portfolio diversification and non-traditional return sources, the investment team at Stanford Brown has, over the past three years, developed a suite of alternative and quantitative investment strategies designed to meet the needs of a broad range of clients. This includes both single and multi-strategy hedge funds as well as traditional equity funds that deploy similar techniques and trading signals as quantitative multi-strategy hedge funds. The inclusion of these quantitative strategies can offer potential diversification benefits for investors and also decreases the key man risks associated with sourcing and relying on skilled portfolio managers, particularly in a world of data proliferation and rapidly changing market dynamics.

By Joseph Nakhoul, Investment Research Analyst

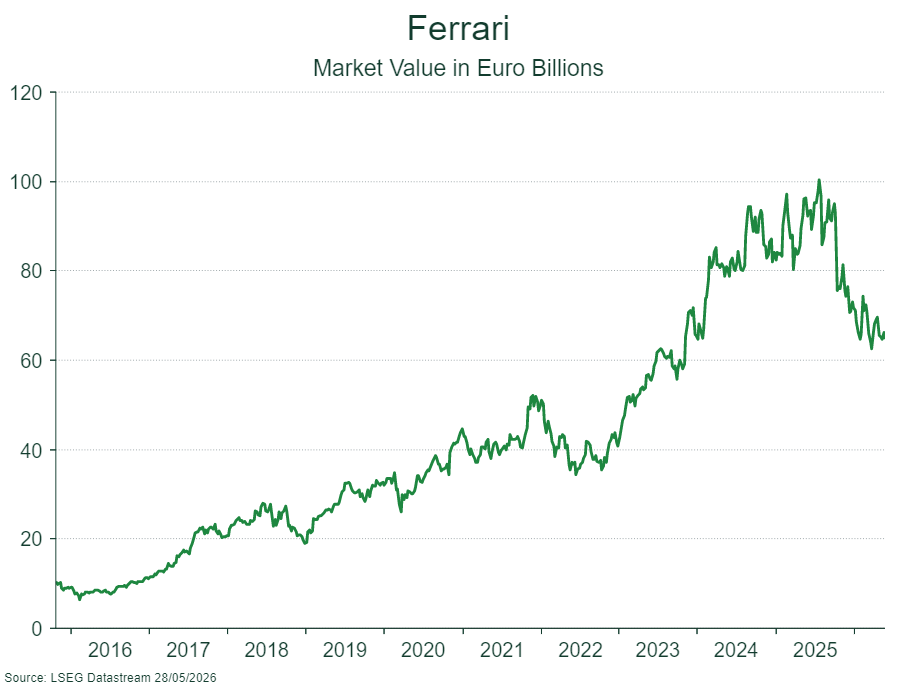

Ferrari Gets Luce

In a move that has sent shockwaves through the automotive world, Ferrari has officially unveiled the Luce, its first-ever production battery-electric vehicle (EV). Revealed this week in Rome, the Luce is not only the brand’s first zero-emissions car but also its first-ever four-door, five-seat sedan. The name, which translates to “light” in Italian, signifies a radical departure from the mechanical violence of the brand’s internal combustion engine past toward a philosophy that embodies the weightlessness and clarity of light.

While the Luce boasts staggering performance figures—including 1,035 horsepower from its quad-motor, all-wheel-drive powertrain, the reaction from long-time fans and the media has been polarising. Within 24 hours of its debut, Ferrari’s stock price plummeted by 8.4% in Milan, reflecting a significant lack of confidence from investors and analysts. Its market capitalisation has fallen by around a third since October, after an investor day where projections of future growth disappointed.

The Luce’s unconventional appearance is the result of a multi-year collaboration between Ferrari’s internal teams and LoveFrom, the creative collective founded by former Apple designers Sir Jony Ive and Marc Newson. The exterior features a two-tone body designed to look like a glass passenger cell sitting within a distinct shell of bodywork. Avoiding the muscular curves of traditional Ferraris, the Luce has the lowest drag coefficient in the company’s history.

The interior has been described as a “TARDIS,” offering unprecedented spaciousness for five passengers. Surprisingly, despite the Silicon Valley influence, the cabin rejects the industry trend of wall-to-wall touchscreens in favour of tactile, physical controls, including mechanical buttons and switches designed to click with high precision.

The Luce is a technical powerhouse with its 122 kWh battery pack serving as a structural element of the chassis, contributing significantly to its torsional rigidity. The battery provides 500 kms of range from a single charge. Ferrari claims the sedan can sprint from 0 to 100 km/h in just 2.5 seconds, reaching a top speed of over 310 km/h. To address the loss of the signature V12 engine roar, Ferrari engineers developed a patented sound system. The system uses accelerometers to capture electromechanical vibrations from the axles, which are then amplified, much like an electric guitar, to inform the driver of torque changes.

The media and enthusiast response has been swift and sometimes brutal. Former Ferrari Chairman Luca di Montezemolo led the charge, stating that the car risks the “destruction of a myth” and jokingly suggesting that “at least the Chinese won’t copy us”. On social media, some critics compared the car to an “Apple mouse on wheels,” while others lamented that founder Enzo Ferrari would be “spinning in his grave”. However, the media has also noted some praise for the car’s bold direction. Some reviewers called the design “different but stunning” and “phenomenal” for its modern, stylish approach to the EV segment.

Priced at approximately €550,000 (A$900,000), the Luce is aimed at a new generation of wealthy buyers who value global prestige and high-tech luxury over traditional racing heritage. Ferrari CEO Benedetto Vigna defended the project, calling it an “unprecedented vision of electrification” that creates a new segment for the brand. Customer deliveries are expected to begin in the fourth quarter of 2026, marking the start of a high-stakes gamble to see if the Prancing Horse can survive its most radical transition yet.

By Nick Ryder, Chief Investment Officer

Bond Markets Sound the Alarm: Sovereign Yields and What They Mean for Australian Investors

Long-duration government bonds have been selling off across the developed world through May, and the move is not easily dismissed as noise. The US 30-year Treasury yield hit 5.2% on 19 May, its highest since 2007, before pulling back to around 4.97% by 28 May. The 10-year benchmark was at 4.48%. Japan’s 30-year yield hit a record high. The UK 30-year gilt reached its highest level since 1998. Australia’s 10-year government bond yield rose nine basis points over the week ending 22 May to close at 5.07%, approximately 62 basis points above where it sat a year ago, although it has continued to come down this week, sitting comfortably below 5% again.

The selloff has multiple drivers and no single trigger. Geopolitical instability from the Middle East conflict is keeping oil prices elevated and inflation stickier than central banks had hoped. Investors are simultaneously repricing how long rates stay high, how much fiscal deterioration they are willing to absorb, and how much compensation they need to hold long-dated paper against that uncertainty. When nominal yields are rising, real yields remain elevated, and term premia are no longer compressed, the message from institutional capital is consistent: the era of cheap sovereign borrowing is not coming back quickly.

The backdrop that sharpened that view was set in May 2025, when Moody’s stripped the US of its last remaining AAA credit rating, cutting it one notch to Aa1 and joining S&P (which downgraded in 2011) and Fitch (2023) in signalling concern about America’s fiscal trajectory. Moody’s projected the federal deficit could approach 9% of GDP by 2035, up from 6.4% in 2024, with federal debt reaching 134% of GDP. The concerns it identified have only grown since. The House passed Trump’s “One Big Beautiful Bill” in May 2025 by a single vote. The House-passed version was estimated to add roughly $2.4-$2.8 trillion to deficits over 2025-2034, depending on the treatment of interest costs and dynamic effects, with the Committee for a Responsible Federal Budget putting the debt impact at around $3.0 trillion including interest, or $5.0 trillion if temporary provisions were extended. After subsequent passage into law, CRFB’s later estimates put the cost higher still, at $4.1 trillion through 2034 or more than $5.5 trillion on a permanent basis, reinforcing the market’s concern that US fiscal policy remains on an expansionary path with no credible corrective mechanism in sight.

For Australian investors, the global repricing has collided with a domestic tightening cycle that may not yet be complete. The RBA raised the cash rate by 25 basis points to 4.35% on 5 May, its third consecutive hike this year following moves in February and March, fully unwinding last year’s easing cycle. The board voted 8-1 in favour. Headline CPI reached 4.6% in March, the highest since 2023, driven in part by energy costs from the Middle East conflict. Monthly figures for April are down, although the next complete quarterly figure will not be out until the end of July. Underlying inflation on the trimmed mean measure held at 3.3% (in March, and 3.4% for the latest April release), and the RBA’s own forecasts have it remaining above 3% until mid-2027.

Markets still see a meaningful risk of further tightening, although softer labour-market data has reduced conviction around the timing of the next move. CBA economists expect rates on hold from here; Westpac sees two additional increases by year-end.

For Australian investors holding duration, the current environment offers yields not seen in over a decade, but the same inflation and rate dynamics pushing those yields higher also carry real risk for mark-to-market valuations if the tightening cycle extends further than current consensus expects. Yields this week have come down somewhat, offering a level of comfort that recent highs are in. But without a resolution in the Middle East and significant progress on domestic and global inflation, this marker is likely to remain volatile for some time to come.

By Joey Mouracadeh, Senior Investment Director

Latest Podcast

SpaceX & the Rate Rollercoaster

This week on SB Talks, CEO Vincent O’Neill and CIO Nick Ryder tackle the market themes everyone is watching, from the buzz around a potential SpaceX IPO to Nvidia’s powerful earnings result and the broader AI trade. They break down what’s driving valuations, where caution may be warranted, and why diversification still matters in a market increasingly concentrated in a handful of names. The episode also looks at the latest Australian jobs and inflation data, and how that is influencing expectations for the RBA.

Listen on Apple Podcasts

Watch on Youtube: